“If we do not change direction, we risk getting where we are going” – this simple wisdom is supposed to exist as a Chinese saying. However, for Ukraine today it is also a warning against the policy that has kept our country in the downward spiral of economic development over the last decades. When despite the intermittent periods of growth and crises in the end of each such period we find ourselves in a worse situation than before. Although our economy has exceeded the pre-crisis indicators of 2013, it is still far from the levels of 2007-2008 and 1990.

The political evolution of recent decades has been a testimony to the degeneration of the political class and state elites rather than their approach to understanding the ways and the willingness to break the vicious circle of degradation. The first months of the new government team’s activities have confirmed the fears of the Week that the pigs in pokes, which as a result of an unprecedented in the history of Ukraine advertising campaign have been sold this year to a record share of the electorate, have also no systematic vision for solving this problem. Their purpose is only to hold key positions in the current model of rapid transition of the country into a typical “banana republic” in both political and economic sense.

As a result, with each turn of the political and economic cycles, Ukraine not only retains existing ones, but also acquires more and more new features that fall within the definition of a “banana republic”. More than a century ago, it was first applied to the most problematic in both economic and political sense of Latin American countries, and then to the post-colonial states of Africa and Asia.

Let's take a look at the most important of these criteria. “Politically unstable country with economies dependent on export of scarce resources”, “large scale plantation agriculture”, “oligarchy controls the primary sector of economy through exploitation of low-cost labor”, “exploitation of the country’s wealth is ensured by collusion between the state and prevailing economic monopolies, when the profits received from the private exploitation of public lands are a private property and the debts are the financial responsibility of the state treasury, “low domestic investments and dependence on the foreign ones”, “chronic budget deficit, soft national currency and high debts in foreign currency”, “society with extraordinary social stratification”, “ large impoverished class of employed people and plutocracy of the ruling class”, “total officials’ corruption”, “political turbulence, power changes often as a result of upheavals”, “other states or organizations have significant political influence”. It is more difficult to find significant differences than similarities with modern Ukraine.

Adding to this the weakness of the ruling political and business elites, their lack of national identity sense and awareness of a larger historical mission, the use of their opportunities to appropriate and often siphon as much of the national wealth as possible off from the country, and the picture is almost complete. It is very difficult for such a country not to become a prey for others, not only states but also financial and economic structures. It becomes naturally helpless in the foreign policy arena and can only be the object the fate of which is entirely dependent (not affected, as in the case of other countries) on the position of those states that have a conscious national concern, a sense of own identity and understanding of long-term priorities.

RELATED ARTICLE: The great balancing act

Getting out of the “banana republic” trap is impossible through the gradual evolution. A young “banana republic” can only grow to a mature “banana republic”, and a mature to an old one. Breaking the vicious circle is only possible due to volitional actions, a purposeful policy of changing the development paradigm. The evolution, or rather the degradation, of a “banana republic” and the increase in contrast with successful states can only be an impetus for the emergence of such a will and an increase in the number of people interested in it. The transition of such countries to another model of development requires a radical, revolutionary change in public policy and elites. And the core principal of the breaking out of the “banana republic” vicious circle on the path of the “welfare state” development is always the change of economic policy. Otherwise, any revolutions or changes in the political elites will be interpreted simply as temporary links, inherent by the definition to “banana republics”, of political instability and power change as a result of the coup.

Defenseless economy

The vicious circle of the “banana republic” is always based on the country's economic weakness and underdevelopment. It is poverty that creates and reproduces industrial backwardness, corruption and political degradation. And these phenomena, in turn, tend to further conserve, and even deepen poverty and economic backwardness. Under the experimental conditions of “closed space”, this situation sooner or later could probably lead to the evolutionary development of the “banana republic” economy due to the emergence and growth of higher value-added industries and the creation of conditions for improving living standards.

This is how the first capitalist and industrialized countries, which today are considered the benchmark, developed. However, if there are no experimental conditions of “closed space”, the economy of any country develops in relation to the economies of others. And economies that began to develop on equal footing prior to those that came later subordinate them. The structure of weaker economies is always selected for the needs of the stronger ones. And it is quite natural that the most attractive, most profitable and dynamic sectors are concentrated in stronger economies, and the worse ones remain in their weaker counterparts. Furthermore, “degrading” political and social set of “banana republics” is the condition and consequence of such economic subordination. It is simply impossible to get rid of it and increase the “banana republics” economic and political development and the living standards of most of their inhabitants without creating mechanisms to protect and stimulate an economy which are capable to level out the artificial advantages (not natural ones, but predetermined by earlier development) of the countries with advanced economies or their high-yield sectors. Without economic nationalism policy, states that are poor and underdeveloped in political and social sense will never be able to become wealthy and developed. And their economy will always be just a subordinate supplement with industries selected outside.

The Ukrainian economy of recent decades is a vivid illustration of subordination to the economic interests of other countries. And our degradation spiral is the direct consequence of the fact that instead of fostering and protecting our production in high-yielding and highly dynamic sectors that could provide rapid economic growth instead of decline, Ukraine has, over the decades, allowed other countries to earn money here for the development of their economies and industrial sectors. Instead, in exchange for a virtually insecure economy and an open domestic market, we have received nothing in the markets of more aggressive countries, especially those that have been actively pursuing the policies of economic nationalism all these years.

Despite the stereotypes that the Ukrainian economy is suffering from a reorientation of trade with the West, trade with the East, or more specifically, the Asia-Pacific region or a group of so-called Far Eastern Tigers, has caused us much more damage. The Ukrainian Week has already drawn attention to the virtually colonial model of our trade with China, the largest economy (in purchasing power parity) and the world factory of the 21st century (see “Colonial Imbalance”, № 9/2019 and “Starting with China”, № 11/2018).

Ukrainian manufacturers of finished commodities have virtually no access to the Chinese domestic market. Instead, from the Middle Kingdom only since the crisis of 2008–2009, from which our economy, and especially industry, still cannot recover, $ 60.8 billion of goods have been imported to Ukraine. Since then, we have been exporting mainly $ 22.5 billion of raw materials there and the total trade deficit with China in 2009 – the first half of 2019 reached $ 38.3 billion.

The situation is similar, albeit on a smaller scale, with other APRs (Japan, Korea, Taiwan, Vietnam, Philippines, and Thailand). Until recently (and some others still have), they have pursued a policy of rigid economic nationalism and restricted access to their domestic markets for finished goods from other countries in order to support and protect their own producers. Meanwhile, Ukraine has remained virtually defenseless against the influx of finished goods from the high-yielding and dynamic industries of these countries while supplying them mainly raw materials, and what is more in much less quantities. As a result, it has a chronic multiple trade deficit with these countries, which among other things limits the concentration of domestic financial resources for the development of the Ukrainian economy. For example, imports of goods from Japan in 2018 ($ 737.4 million) exceeded our exports ($ 231.9 million) by more than three times. The same ratio is observed in trade with Vietnam ($ 414.6 million in imports versus $ 132 million in sales of Ukrainian goods to this country) or Taiwan ($ 252 million versus $ 68.8 million). Imports of goods from Korea ($ 436.6 million) also exceeded shipments of our goods to it ($ 327.4 million) by more than $ 100 million.

However, it is not only the deficit but also the trade structure that gives Ukraine the role of a country specializing in sectors with lower added value and growth dynamics. Consequently, it preserves poverty and economic backwardness.

For example, imports to Ukraine from China, Japan, Korea, the Philippines, or Taiwan in 2018 by 98-100% consisted of manufactured goods. At the same time, 55% of Ukrainian exports to China are ore and grain; another 26% are sunflower oil and oilseed meal (a by-product of sunflower oil production). Machine building products accounted for only 10.2% (according to the latest data, almost twice less since the beginning of 2019). In the Ukrainian deliveries to the Philippines, the share of grain reaches 96%, while the import from this country to Ukraine by 98.5% consists of industrial products, including almost 90% from the field of mechanical engineering. Ukraine mainly supplied to Korea grain (53.6%), ore (23.2%) and raw wood (5.6%). Machine-building products accounted for only 2.6% of total deliveries, and metallurgical semi-finished products – 8%.

The structure of Ukrainian deliveries to Japan is not much better: 57% make up ore and grain; another 30.7% are tobacco, machine-building products account for less than 1% of our exports. 90% of Vietnamese deliveries to Ukraine consisted of manufacturing products, while Ukrainian deliveries to Vietnam were mainly ore (28%), oilseed meal (18.4%) and meat and its by-products (16.7%). The share of ferrous metallurgy products was only 7.8%, mechanical engineering made up 6.3%.

At the same time, Ukraine every year is increasingly flooded with Asian engineering products, electrical engineering and a large number of other consumer goods. According to the 2018 data, Chinese imports to Ukraine are 53.4% of machine-building products. The situation is similar with other countries in the Asia-Pacific region (APR). For example, the share of mechanical engineering products in imports of Ukraine from Thailand makes up 50%, Malaysia – 52%, Korea – 59,7%, Vietnam – 65,1%, Taiwan – 70%, Japan – 81,1%, the Philippines – 89,6%. As a result, total imports of machine-building products from only these countries in 2018 amounted to $ 5.66 billion. At the average annual rate of the NBU, this is UAH 153.9 billion, which is half as much as all Ukrainian manufacturers sold their products in the domestic market (UAH 102.9 billion). The situation is similar and even worse in the light, furniture, and glass industries, in the segment of products from ceramics and stone, gypsum and cement, which could be a springboard for the development of Ukrainian small and medium-sized businesses and generator of jobs in regions with high unemployment.

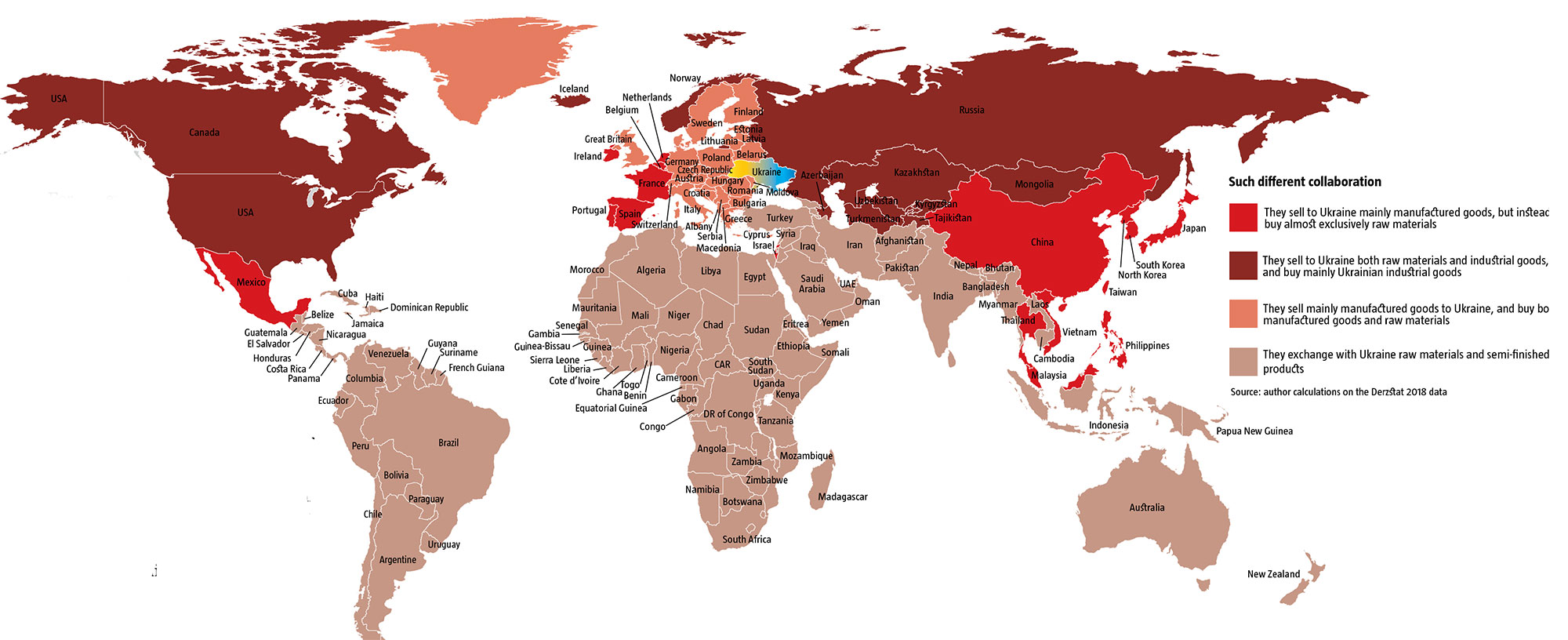

According to our analysis of the commodity structure of Ukraine's foreign trade in the cross section of different countries (see map), there are four types of partners in general. Of the first type are the countries that supply finished goods to Ukraine and buy our raw materials and in much smaller volumes semi-finished products. Such trade causes the greatest damage to the domestic economy. And the leading role here is played by the countries of the Asia-Pacific region. The second group consists of countries that supply both raw materials and finished goods to Ukraine, but instead buy mostly manufactured goods. The third group consists of countries that supply mainly finished goods to Ukraine, and buy both raw materials and manufactured goods. And the fourth type is the countries with which Ukraine exchanges mainly raw materials and to lesser extent industrial semi-finished products.

And next thing you know that, despite the widespread notions, trade with developed countries of the EU and North America is less disproportionate for Ukraine than with the countries of the Asia-Pacific region. The access of our goods to the western markets is easier, and the level of their aggressiveness in the production sphere and the competitiveness of their manufacturing industry are much lower, thus the dangers for Ukrainian production are much smaller than those of the Asia-Pacific countries.

For example, the share of machine-building products in Ukrainian imports from the EU is only 36.4%, which is significantly less than in imports from the countries of the Asia-Pacific (let us recall that it is 50-90%). And in absolute volumes ($ 4.3 billion), the volume of imports of engineering products from the EU today is significantly inferior to deliveries to the Ukrainian market of engineering products from eight Far Eastern countries ($ 5.66 billion). Not to mention the dynamic increase in supplies from the Asia Pacific region.

Instead, the share of mechanical engineering in Ukrainian exports to the EU is 15.2%, which is significantly higher than in the structure of Ukrainian exports as a whole or even more than our sales to the countries of the Asia-Pacific region. At the same time, both the volume of export of engineering products to the EU and its share in our exports to the EU are growing quite dynamically. This is evidenced by the dynamics since 2013. From $ 2.16 billion, then, the volume of exports of Ukrainian mechanical engineering products increased to $ 3.06 billion in 2018, and the share of all Ukrainian exports to the EU increased from 10.6% to 15.2% during this time, which is almost half as much. It continues to grow. Moreover, the volume of Ukrainian exports of mechanical engineering products to the EU ($ 3.06 billion) and imports of such goods from the EU ($ 4.3 billion) are broadly comparable. Other manufactured goods in our EU supplies make up another 51.2%. Instead, only a third of Ukrainian exports to the EU account for industrial (ores, stones) and agricultural (grain, oilseeds, etc.).

It’s a different matter that the product structure is rather uneven across the EU. Co-operative relations developed mainly with Germany and the Visegrad Four countries. Exports of domestic engineering products increased to a lesser extent to Romania and the Baltic States. The export geography of other Ukrainian industrial products follows these directions. At the same time, far-flung EU countries such as France, Belgium, Spain, and especially Portugal and Ireland, almost do not buy Ukrainian finished goods, limited to small amounts of metallurgical semi-finished products or crude sunflower oil.

At the same time, Russia, along with most Asian CIS countries, belongs to the group of our trading partners whose supplies to Ukraine are dominated by raw materials (mainly due to fossil fuels, but not only them). However, the volume of Ukrainian exports to the market of the Russian Federation and other Asian CIS countries, on the contrary, has fallen sharply over the years. The week has already analyzed the causes of this decline in a publication specially dedicated to this issue. It is not about ephemeral "refusal of Ukraine to trade in traditional markets", but about the reduction of dollar prices, demand and total capacity of Russian market and other gas and oil dependent markets, in the first place of the Russian Federation. And also a long-term policy of import substitution, especially in the Russian machine-building industry, which took place long before the Revolution of Dignity and the beginning of the Kremlin's aggression against Ukraine.

Oddly enough, the group of countries that supply not only finished goods to Ukraine but also large quantities (and in some cases, mostly) of raw materials, buying on the other hand there mainly industrial ones, include the USA and Canada in America and Norway and Iceland in Europe. With the latter two, everything is simple: the lion's share of deliveries from there is fish (70.3% of imports from Norway and 94.1% from Iceland). And Ukraine mainly sells mechanical engineering products (37.2% of our exports to Norway and 47.2% to Iceland) and manufacturing production (44.1% of our exports to Norway and 52% to Iceland).

Imports from Canada ($ 333.1 million), though several times higher than our exports there ($ 78.1 million), are by 49.2% made up of fossil fuels and by 10.8% more of fish. The share of mechanical engineering products of Canadian imports to Ukraine last year was only 15.2%. At the same time, the share of mechanical engineering products of Ukrainian exports to this country reached 16.3%, and of manufacturing production in total reached more than 99%. In the structure of imports into Ukraine of goods from the USA, the share of raw materials is lower (37.4%) than from Canada, and of the products of mechanical engineering is, on the contrary, higher (40%). At the same time, Ukrainian exports to the United States now account for 97% of manufactured goods, albeit with different processing depths. The largest share is made of ferrous metallurgy (63.6%), another 12.4% is metal products, and 7.9% is mechanical engineering products, 5.2% is food industry.

RELATED ARTICLE: The new multivectoral economy

There is only one country on the American continent, which, while supplying mainly mechanical engineering products to Ukraine, imports mainly raw materials from Ukraine, it is Mexico. Deliveries of goods to Ukraine from Mexico for 65.6% consist of products of mechanical engineering and 88% of manufacturing production in total. At the same time, Ukrainian exports to Mexico are almost by 50% made up of ore and agricultural raw materials (grain and oilseeds) and only 5.3% of mechanical engineering products.

Unlocking of economic development in Ukraine demands a new look at trade and economic relations with the outside world. The approach to trading cooperation with different partners needs to be changed considering self-interest in the first place. The focus should be on developing our own production and domestic market. If we still need the currency for a long time to cover the critical imports of certain types of raw materials and investment goods needed to modernize the economy, then we can sell for some time traditional export goods, albeit mostly raw materials. But you need to take care of the domestic market, restrict access of other countries to it. Make it dependent on opportunities for similar access to attractive segments of their market or other advantages for Ukraine. Hindering access to the domestic market for Far Eastern importers of finished industrial goods, which are today virtually blocking the development of a number of manufacturing industries in Ukraine, we have a considerable chance of substantially increasing domestic production at least for our own needs.

Follow us at @OfficeWeek on Twitter and The Ukrainian Week on Facebook