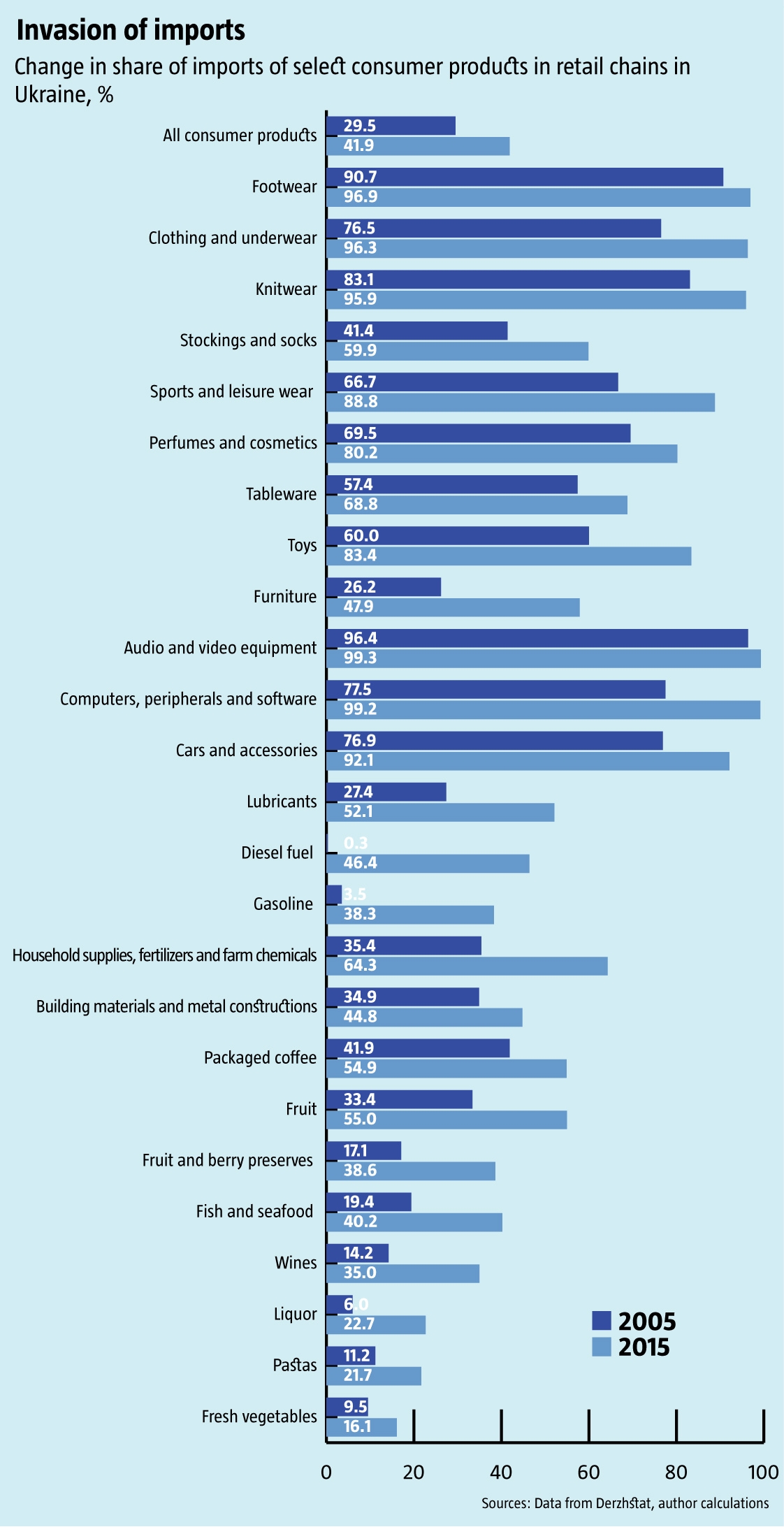

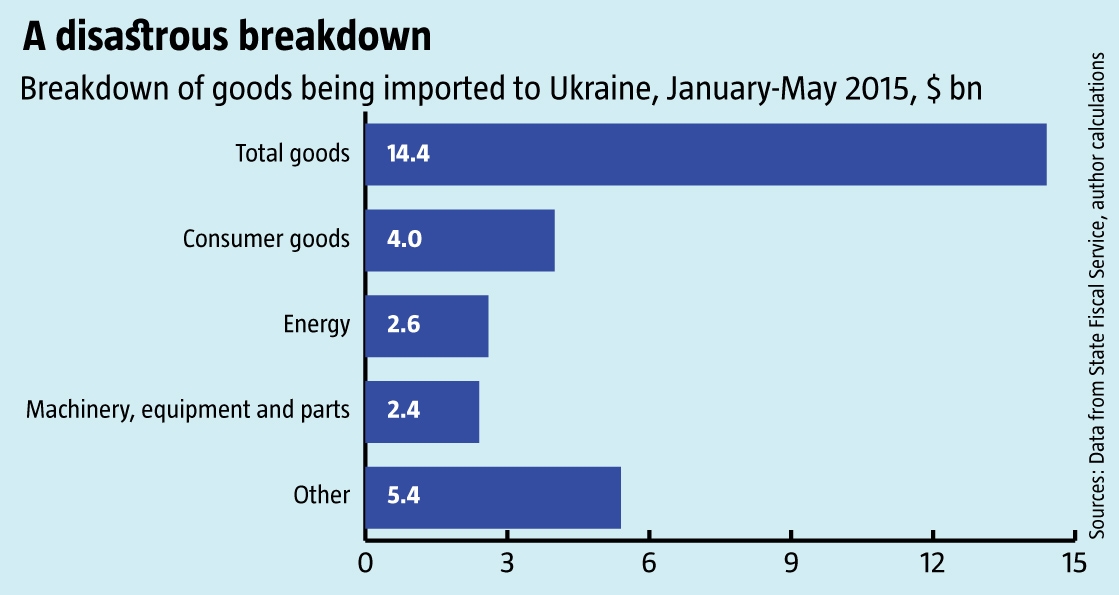

Ukrainians spend close to UAH 1 trillion on imports every year. Last year, officially US $37.5bn was bought, although a good portion of imports is brought in on fixed contracts with artificially low prices or are simply contraband. What’s more official figures from Derzhstat show that the proportion of imports to Ukrainian-made consumer goods in retail networks has tended to grow over the last 10 years. Where in 2005, the share of all imported goods sold by Ukrainian retailers was 29.5%, by 2013, it was up to 42.8%, nearly half again as much.

In the last two years, domestic products have won back a tiny share of the market, inching up from 57.2% to 58.1%. But when we consider that this tiny drop in imported goods took place at a time when the hryvnia plunged to a third of its former value, meaning that foreign-made goods tripled in value, it’s clear that this represents a serious threat, not just to a rapid recovery, but to real growth in the share of Ukrainian-made goods in the foreseeable future.

RELATED ARTICLE: Aircraft building and aviation industry in Ukraine

Curiously enough, the share of critical imports—energy and raw materials—has been shrinking year after year, as has spending on imported machinery and equipment necessary to modernize the country’s economy, while foreign-made consumer goods have steadily strengthened their positions on Ukraine’s domestic market. Replacing these goods with Ukrainian-made ones would have a major positive impact on the country’s economy, which has continued to decline—the volume of goods and services produced per capita remains well below both 1991 and 2008 levels. It would also provide jobs for millions of Ukrainians who are unemployed today.

The logic of import substitution, Ukrainian-style

The need for import substitution in Ukraine has no relationship with the idea of autarchy or self-sufficiency, which is common of totalitarian regimes that want to isolate themselves and oppose the world around them. It should be based on common sense and on a need to mitigate the excessive dependence of the domestic market on imports of an enormous range of consumer goods.

In 2015, Ukraine’s workforce, not including the occupied territories, amounted to 19.9mn people of working age—excluding those who are studying or cannot work for health reasons—, and 0.7mn people of pensionable age who were still working. The rest, one way or another, is simply hidden unemployment, which can currently be estimated at about 10mn of able-bodied Ukrainians. The fact that they somehow manage to find part-time, temporary or irregular work for pay, which Derzhstat, the statistics agency, categorizes as “self-employed” does not really change the reality.

In the current economic situation, setting up a greenfield export-oriented business is hard for small businesses, and even for a good chunk of medium ones. This is especially true if it involves entering markets that are distant and not traditional for the particular sector. This process needs to be linked to getting Ukraine plugged into the global chains of transnational corporations and to the individual success of big domestic business, and a portion of medium ones as well.

RELATED ARTICLE: The prospects of nuclear power generation in Ukraine

But historically, the success of Ukrainian SMEs, especially those that are start-ups, has the best chances when started precisely with winning a share of the domestic market. This generally includes both setting up new greenfield manufacturing and transferring part of a partner’s technology and manufacturing facilities to Ukraine under various forms of collaboration, be it on a cooperative or a license basis. Once a business is successful on the domestic market and has developed some “muscle,” such domestic firms can also try entering foreign markets.

This kind of strategy should go hand in hand with the process of European and global corporations setting up subsidiaries in Ukraine and should play the key role in providing a new, populous layer of independent local businesses. Betting exclusively on the production capacities, especially export oriented ones, of transnational corporations or on tolling schemes is dangerous in the long run: since such corporations are not tied to Ukraine in anyway except for reliable flows of profits from their facilities here, they will be the first to move those facilities to another country the minute the global situation changes.

Promising niches

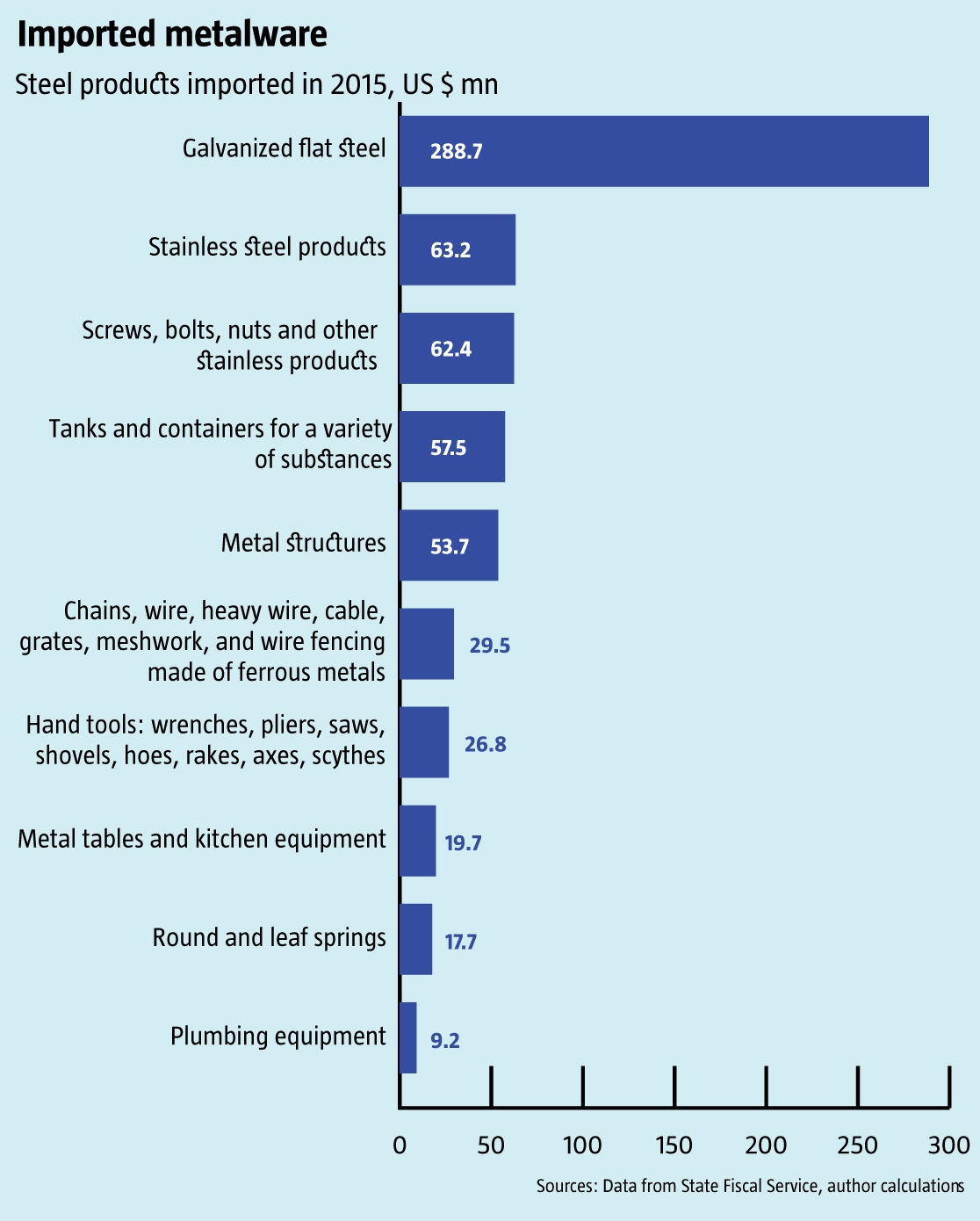

Ukraine continues to be a major exporter of semi-finished casting products that it is having an ever-harder time selling, at the same time as finished steel  products with a much higher added value are being imported in growing volumes. What’s more, these suppliers are from countries where the cost of labor in the steel industry is far higher than in Ukraine (see Imported metalware). Meanwhile, the country’s steel magnates, aka oligarchs, are in no hurry to expand the scale of processing in their facilities, which has led to growing unemployment in the industrial belt of Ukraine’s southeast.

products with a much higher added value are being imported in growing volumes. What’s more, these suppliers are from countries where the cost of labor in the steel industry is far higher than in Ukraine (see Imported metalware). Meanwhile, the country’s steel magnates, aka oligarchs, are in no hurry to expand the scale of processing in their facilities, which has led to growing unemployment in the industrial belt of Ukraine’s southeast.

More recently, Ukraine has been increasing its exports of light industrial goods and furniture to European markets on the basis of toll manufacturing. Clothing sold abroad in 2015 alone reached nearly US $500mn, and a few hundred more million in furniture, toys and sports equipment was shipped out. Stable demand for these Ukrainian-made goods testifies to the highly competitive capacities of domestic enterprises in filling orders. Nevertheless, the share of imports of light industrial products remains dominant on the domestic market.

Indeed, the share of Ukrainian-made clothing out of cloth has collapsed from 23.3% to 5.7% in the last 10 years, the share of knits has plunged from 16.9% to 4.1%, and the share of footwear has dropped from 9.3% to 1.1%. Even the market for stockings and socks, where domestic manufacturers remain among the strongest in light industry, the share of imports has jumped from 41% to 60% in the same period. Based on their officially declared value, which is typically artificially reduced to cut down on import duty, clothing and accessories alone worth US $340mn were imported in 2015, plus another US $193mn in footwear.

Ukrainian makers of cosmetics and perfumes are also sharply losing market share, losing 33% over the last 10 years, down to 30.5% and 19.8% of the total market for these goods. And yet, the volume of imports of cosmetics, perfumes, personal care products like soap, shampoo and tooth paste was over US $470mn, even at the height of the economic crisis in 2015.

There is also tremendous potential for import substitution in the fuel and energy complex (FEC). This year, Ukraine will likely spend US $6-7bn on this. The process of substituting natural gas has been going on for several years now and has been given a real boost by increasing the price for domestically extracted gas to import levels. Meanwhile, to increase the share of domestic refining, this is the best time to take advantage of the situation as the world market for black gold undergoes a major redistribution. The idea would be to offer one or more oil-producing countries that would like to push Russia out of the European market to partner in an oil refinery project with considerable depth of refining in Ukraine.

Flourishing with the farm sector

Even as Ukraine has justified claims to status as an “agricultural superpower,” it remains a major importer of a slew of foodstuffs with significant added value. Fully 16% of its fresh vegetables, nearly 25% of its canned vegetables, 40% of its fruit preserves, and 55% of the fresh fruit sold in supermarket chains all come from abroad. Similarly, 55% of packaged coffees and 30% of teas are imported, along with 23% of spirits and 35% of wines, shares that have doubled and tripled over the last 10 years.

Even as Ukraine has justified claims to status as an “agricultural superpower,” it remains a major importer of a slew of foodstuffs with significant added value. Fully 16% of its fresh vegetables, nearly 25% of its canned vegetables, 40% of its fruit preserves, and 55% of the fresh fruit sold in supermarket chains all come from abroad. Similarly, 55% of packaged coffees and 30% of teas are imported, along with 23% of spirits and 35% of wines, shares that have doubled and tripled over the last 10 years.

This massive trend towards more and more imports of food is in the face of considerably higher prices compared to domestic products and is again a reflection of how Ukrainian producers are ignoring specific segments of this market. Ukraine is thus a major importer in the food business: extracts and essences of coffee and tea worth US $134.4mn; pure ethanol worth US $122.8mn, beers and wines worth US $85mn, chocolate worth US $70.5mn, processed vegetables worth US $46.6mn, ready-made sauces and spices worth US $45.5mn, and feed for livestock worth US $144mn. At the same time, a significant share of imported fresh vegetables, worth US $48.8mn, is in part due to a domestic greenhouse business that is underdeveloped, while imports of apples and pears worth over US $23mn is related to underdeveloped infrastructure for keeping such produce in Ukraine.

With energy conservation on the rise, new opportunities for import substitution are becoming available, increasing demand for energy-saving equipment over traditional versions substantially. For instance, in 2015, central heating furnaces worth US $37.9mn were imported to Ukraine, as well as US $31.4mn worth of radiators, and US $23.6mn worth of high-efficiency light bulbs. This growing market offers opportunities to set up local manufacturing, which is good for both existing manufacturers and new ones, specifically to set up cooperation with foreign companies. Nor is much being done to take advantage of the potential to set up local production of durable consumer goods, such as household appliances, computers, telephones and smartphones, and passenger cars.

At the same time as the sector for outsourced IT services has been booming for the last 10 years, the share of computer technology, peripherals and software being produced domestically collapsed almost entirely, going from 22.5% in 2005 to a marginal 0.8% in 2015. Even at the officially declared prices in import contracts, foreign computers, mobile phones and spare parts were worth US $1bn in 2015. An additional US $660mn worth of electronics were imported. In the last decade, the share of automobiles assembled in Ukraine has plunged from 23% to 8%, with US $824mn worth being imported in 2015 alone. Rubber tires and tire casings worth over US $250mn are brought into Ukraine from abroad every year.

Domestic SMEs are more than capable of substituting with their own products in these markets by working with foreign manufacturers of equipment under license, which would establish an area of potential operations for hundreds of new SMEs and generate tens if not hundreds of thousands of new jobs.

Meanwhile, Ukraine’s farm sector is currently developing based on the widespread import of technology, equipment, fertilizers, seed, and plant protection means. Even in crisis-ridden 2015, over US $2bn of this kind of goods was imported according to official data. In fact, some segments are nearly entirely dependent on imports, which not only suggests that the domestic market is being completely ignored, but also represents serious risks to stable growth in Ukraine’s AIC, although it is the largest and one of the most promising sectors in the domestic economy. In the fertilizer market, which is worth US $708mn, there is a Russian-Belarusian monopoly on a slew of positions, especially potassium, phosphates and potash-phosphate compounds. Yet, as the domestic farm sector continues to grow, it will need this kind of product in greater volumes.

RELATED ARTICLE: Ways for Ukraine to become self-sufficient in the energy sector: Is this possible?

What’s even more promising is the modernization and replacement of depreciated farm equipment and machinery, without which the sector’s potential will never be reached. In 2015, farm equipment worth some US $600mn was imported, including US $229.3mn in tractors, US $106.6mn in grain harvesters, US $70.4mn in seeders and mowers, and US $22.4mn in plows and harrows. Today, the market for this equipment is already highly competitive. For instance, Belarus and the US are jockeying for top place in supplying tractors, with each of them boasting around 25% market share, followed by suppliers from several EU countries—the Netherlands, Germany, France and Poland—and China. The Ukrainian market is clearly a good one to invest in, as its potential for dynamic growth is already evident. Clearly, some of these manufacturers might be prepared to set up production lines in Ukraine and to gradually expand their market share of locally-made parts.

Get over your complexes

There is a widespread and dangerous maximalism in Ukraine today, where import substitution is being rejected because domestic producers are not able to offer either exclusive or innovative products that are better than the best analogs elsewhere in the world or at least at their level. This kind of attitude has already caused Ukraine considerable harm as it treads water industrially. Meanwhile, a slew of Asian countries that just 10-20 years ago were in worse shape than Ukraine managed to get their hands on licenses and technologies to produce items that were devised in developed countries and are not the latest any more. This ensured them rapid expansion of manufacturing capacities, more jobs and higher incomes for their citizens, which in turn stimulated a wealthier consumer market and more muscular business. In a country where effectively every second adult has no official job, localizing just about any kind of manufacturing that can substitute for imports would be a great boon.

Here, we also have to consider another “complex” that is common among Ukrainians, and that is prejudice against goods made in their own country as being ipso facto worse than any imports. This creates an illusion that Ukrainians themselves are unable to produce anything of substance and therefore have no right to a decent living standard and lifestyle. Those who actually buy “Made in Ukraine” products vehemently disagree with this position.

The role of the state

The bottom line is that import substitution cannot possibly take place using traditional measures such as protectionism based on discrimination or prohibitive import duties. Ukraine’s international commitments and its enormous dependence on exports mean that the country’s domestic suppliers would run into serious problems. Artificial protection would also have a long-term negative impact on the overall competitiveness of the domestic economy.

On the other hand, the government can provide incentives for import substitution by supporting companies in those sectors where they can quite easily compete on the domestic market with foreign suppliers. It can also influence outside suppliers by incentivizing the establishment of local production facilities, starting with simply assembling final goods and eventually increasing the level of local manufacturing.

For instance, the government can offer leasing and crediting programs to its citizens and companies registered in Ukraine that only cover the assembly or production of goods in country. It can also offer hryvnia-denominated loans on the same terms and conditions that foreign competitors get them. Tax holidays for new businesses or for new projects by existing firms are popular form of incentive. Finally, red tape needs to be minimized so that issues related to permits, land allocation, utility hook-ups for new production facilities and so on are handled quickly and effectively.

RELATED ARTICLE: Small and medium business in Ukraine: current role and problems, prospects

Last but not least, there needs to be a well-thought-out, high quality policy for keeping people informed and for training potential entrepreneurs, managers and production workers for future import substitution projects. All too often, potential entrepreneurs and employees alike have no idea how to make things happen for themselves without emigrating. At a certain stage, it makes sense for the state and international foundations and organizations that have resources for this purpose to provide funds to invite managers and other specialists from abroad to consult and share knowledge for the necessary production facilities to be launched and established in Ukraine.

And there’s more that can be done: the government can also build greenfield facilities, manage them until they are profitable, and then sell shares on the stock market or auction off entire complexes. Any money earned can be reinvested in repeating the same scheme to develop import-substituting manufacturing. In the end, all these measures and others that have not been mentioned should be used alone and in combination for the maximum possible impact.

Domestic production of many products to replace simpler imports or imported goods that are in serious and growing demand—through developing the farm sector and energy conservation, modernizing infrastructure, and so on. By providing jobs and adding consumers with cash to spend will increase demand internally and expand the domestic market considerably, which will, in turn, increase GDP and tax revenues in the budgets of various levels of government, and generate more jobs in the service industries. The multiplier effect is potentially enormous for Ukraine.

Translated by Lidia Wolanskyj

Follow us at @OfficeWeek on Twitter and The Ukrainian Week on Facebook