The tender for the privatization of Odessa Port Plant (OPP) was much-anticipated. The preparations took nearly a year. It was supposed to become the first in a series of large enterprises denationalized after the Maidan, to provide proof of the new government's loyalty to the principles of market economy, transparency and efficiency, and to demonstrate to international investors that the transformations taking place in the country are irreversible and are being implemented steadily. Unfortunately, this did not happen. When the deadline for submitting the bids expired, it turned out that there were none.

The answer to why this happened is simple: OPP was not ready for privatization.

First of all, the plant did not have adequate managers. The arrest of the head of OPP's Supervisory Board Serhiy Pereloma and of the First Deputy Chairman of the Board Mykola Schurikov accused of embezzling its assets worth hundreds of millions of hryvnias is a sign that this state-owned company, as in many similar cases, has most likely bred too many parasites. Solving this problem, a typical one for the country, had to be an indispensable part of preparing OPP for privatization. Ihor Bilous, Head of the State Property Fund, said that the arrest of the plant's managers could not disrupt the tender. However, embezzlement means that the company's actual financial performance is understated, decreasing its real value and making the plant less attractive to investors.

RELATED ARTICLE: How Ukraine's imports changed over the past 2.5 years

Second, the problem of the company's debt remains unsolved. In mid-2013, entities owned by oligarch Dmytro Firtash supplied natural gas to OPP. This created a debt of $193 million. This amount is still on the company's books as liabilities. Together with $53 million in penalties for delay in payment, this amounts to almost $250 million of financial claims, which Firtash's entities took to the arbitration in Stockholm.

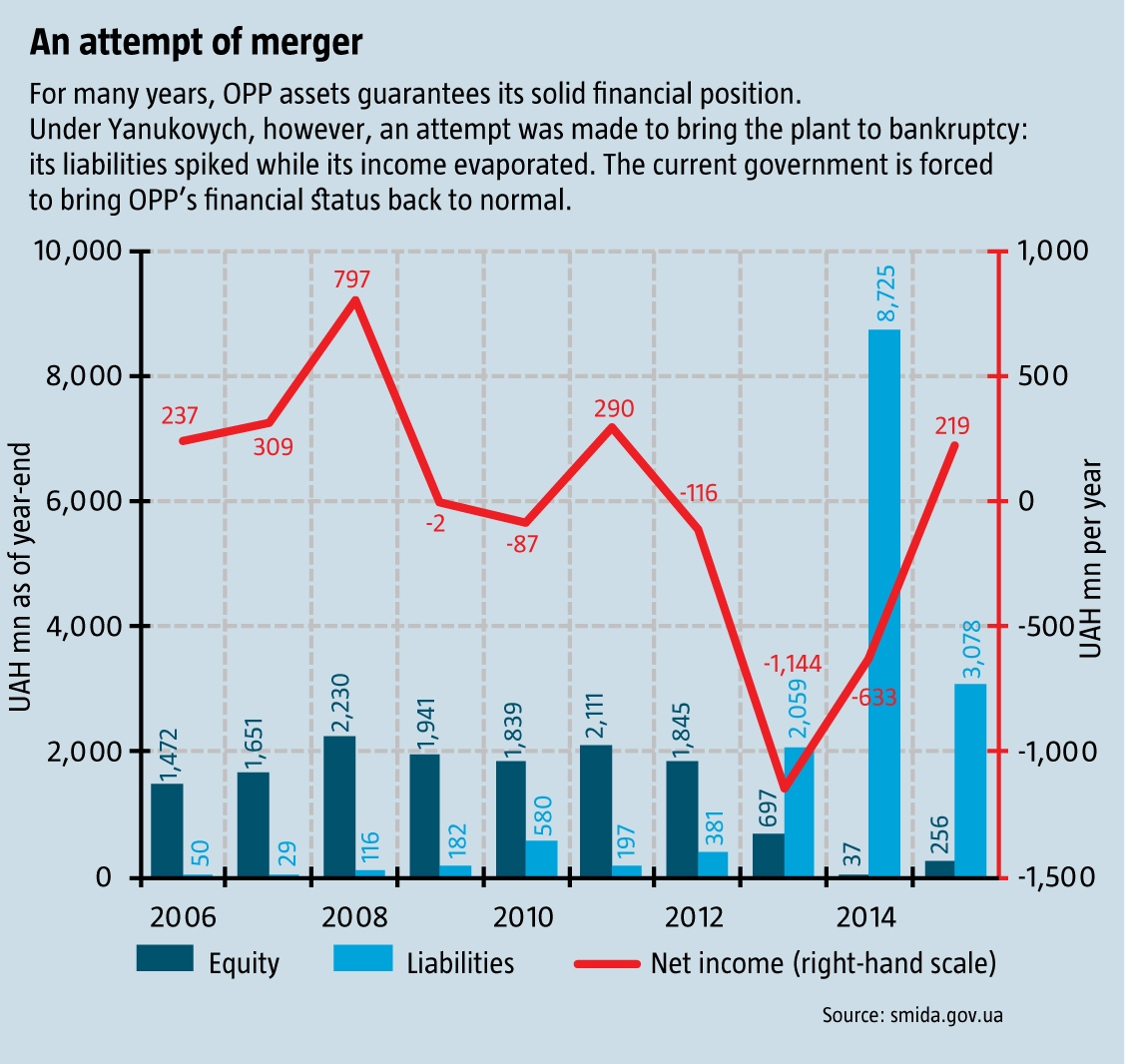

Another side of the coin which no one discusses is why the OPP didn’t take a simple bank loan to buy the gas back in 2013, instead of working directly with the entities owned by Firtash? The company's financial situation has always been strong, so getting a loan could not be a problem. Why did the plant show surprising losses that same year? Why did the net worth of a powerful plant with a solid list of strategic advantages (including ammonia pipeline, location next to the port, and fertilizers handling capacity), which ensured its consistent financial stability, fell almost to zero over just two years? The answer to all these questions is quite obvious: the plant was deliberately being bankrupted and prepared for the forced sale to Firtash in compensation for the artificially imposed debt. This scheme was generated under Yanukovych.

Another side of the coin which no one discusses is why the OPP didn’t take a simple bank loan to buy the gas back in 2013, instead of working directly with the entities owned by Firtash? The company's financial situation has always been strong, so getting a loan could not be a problem. Why did the plant show surprising losses that same year? Why did the net worth of a powerful plant with a solid list of strategic advantages (including ammonia pipeline, location next to the port, and fertilizers handling capacity), which ensured its consistent financial stability, fell almost to zero over just two years? The answer to all these questions is quite obvious: the plant was deliberately being bankrupted and prepared for the forced sale to Firtash in compensation for the artificially imposed debt. This scheme was generated under Yanukovych.

As a result, the company formally owes Firtash money and currently has nowhere to find it to pay off its debt. The SPFU should have dealt with this situation before listing OPP for privatization. There were several possible solutions to the problem: selling these liabilities to other entities, so that the state could gradually deal with them, or taking a loan, for instance, from the Savings Bank (such loan appeared on the OPP books in 2014, but disappeared from there last year). None of these options have been implemented, and the problem remained. According to rough estimates, the real value of the plant is now about $250 million lower than it could be, because the new owner will have to pay off the debts.

Third, there is a much longer information trail also associated with OPP. It starts with the unsuccessful attempt of selling it in 2009, when Nortima LLC controlled by oligarch Ihor Kolomoisky won the privatization tender and was ready to pay UAH 5 billion for the company (over $600 million at the time). However, the tender results were canceled because, as they say, the then Prime Minister Tymoshenko had other plans for it.

RELATED ARTICLE: Transition from oligarch economy to EU membership for Ukraine: how to?

At the first glance, back then the state was wrong to adopt an unprecedented and a very dubious decision. So, Kolomoisky has every reason to expect to win in court. The ligarch is now exercising information pressure on the potential investors by stating his firm intention to challenge the results of this previous tender. It is clear that investors will be reluctant to buy an asset that they could lose only because someone once wanted to buy it. However, one question remains: Why has Kolomoisky not started the proceedings concerning the cancellation of OPP privatization in 2009 to this day? The answer seems to be simple. Under Yanukovych, he had no chances of winning. After the Maidan, OPP received a new management connected to Kolomoisky, owing in no small measure to then-premier Arseniy Yatsenyuk's efforts. It is quite possible that the Kolomoisky managed to siphon off part of the company's cash flows without any privatization, and had no special reasons to struggle to own it officially.

Of all the SPFU failures, the starting price definitely wins the garland. On May 18, 2016, a Cabinet meeting approved that the state-owned stake of 99.6% OPP shares would be sold at the price starting from UAH 13,175 million, or $523 million.

In 2009, when OPP was put up for sale, its starting price was about $500 million. A year earlier, the company earned a record profit of UAH 797 million, which then equaled $151 million. This became possible thanks to the super-high global prices for fertilizers, combined, however, with the high prices for natural gas). If the plant were sold before the crisis, then, given this level of profits, it could easily be sold for $1 billion, or even for $1.5-1.8 billion. But in 2009, when the crisis was in full swing, and the prices for fertilizers and natural gas declined significantly, the value of the plant naturally decreased. Therefore, the starting price determined by the SPFU was more or less fair. The sum of over $600 million that Kolomoisky was willing to pay at that time was slightly lower than the maximum that the government could expect to receive at that time, but given the global situation and the lack of buyers, the price was reasonable (the price was right, but the timing was wrong).

RELATED ARTICLE: The burden of ownership: what assets remain publicly-owned and plans to privatize them

Today, the price for gas and fertilizer is 1.5-2 times lower than the lowest for 2009, and 4 times lower than the highest for 2008. It is clear that the profits earned by OPP in 2008 divided by 4 would today be the limit of expectations, but last year the company did not earn as much (probably due to embezzlement). How could the starting price under such conditions be set at the level of 2009, considering also that seven years ago the plant had no debts, and now it has plenty of them on its books?

According to experts, Swiss investment bank UBS, which advised the SPFU, recommended the starting price of $300 million, a figure that is adequate to the current situation and which, in case of a real competition among the buyers, could increase quite noticeably in the bidding process. But eventually either the Fund or the Government decided for some reason to heed the advice of some "independent appraisers."

The Ukrainian Week already wrote that the enterprises still remaining in state ownership have numerous unsolved problems and difficulties in management. No one is in a hurry to clean this all up, forget about any systematic work. OPP is not an exception. Its problems are further aggravated by the lack of the guarantees of uninterrupted gas supply (which was mentioned as if unintentionally in his comments by the managing director of Firtash's Group DF Boris Krasnyansky, as well as by Bilous). Recently, Ukrtransgaz announced its intention to turn off gas supplies to the plant, but then the problem was allegedly solved. But this is again a typical example for Ukraine, when the oligarchs, acting through officials controlled by them, use infrastructure to pull the plug on other businesses that they don't like. The owners of ArcelorMittal Kryvyi Rih (former Kryvorizhstal) who have been working in Ukraine for 10 years now can cite numerous everyday examples: every now and then Ukrainian Railways would run short of cars to transport their products, or have some problems with railroad tracks, or some difficulties in ports would arise.

Such superficiality of the Ukrainian officials has repeatedly negatively affected the entire country. However, this is not an isolated problem. At the other extreme, it has another huge flaw: literalism and excessive and unbelievable number of formalities. The deep understanding and thorough study of each issue takes time.

The third flaw is the inadequate perception of the situation. We can assume that the starting price of $523 million is a political decision motivated by the active cooperation with the West and the hopes that the very fact of this interaction would help find investors. But for nearly a year now, Ukraine has been unable to resume its cooperation with the IMF, although the demands of the latter are very specific, and the action plan is incredibly detailed. Foreign investors look at the situation more realistically. Meanwhile, no country's officials showed such adequate perception of the situation, at least not in the public information space, until the failure of the OPP privatization tender.

RELATED ARTICLE: Of vouchers and men: Privatization in Ukraine after the collapse of the Soviet Union and its role in the rise of oligarchy

Summarizing the above, Ukraine’s officials should talk (or promise) less, curb their appetites and start working more efficiently, instead of giving the appearance of working. Then, probably, the fourth flaw — lack of communication — could be withdrawn from the agenda. Why the lack of bids for the OPP privatization tender was a disappointment to many? Because the expectations, even those of the insiders, were exaggerated, while the outsiders believed the tall tales that they were being told.

In summary, in order to overcome the chronic problems of the state machine leading to failures such as the OPP privatization, people who have the will for that would have to deal with the law, with corrupt officials, with the poor culture of the civil service, with the oligarchs and their money and, eventually, with time. Is this an adequate task? In general, yes. But not today, because the alignment of forces in the society does not encourage change (for the lack of intellect, energy, and the people aspiring to make a difference). The situation with the OPP privatization once again proves that the oligarchs are too strong, the state is too weak, and the officials are too inadequate.

Translated by Anastasia Asianova

Follow us at @OfficeWeek on Twitter and The Ukrainian Week on Facebook