IMAGINE discovering a one-shot boost for the world’s economy. It would revitalise firms, increasing sales and productivity. It would ease access to credit and it would increase the range and quality of goods in the shops while keeping their prices low. What economic energy drink can possibly deliver all these benefits?

Globalisation can. Yet in recent years the trend to greater openness has been replaced by an enthusiasm for building barriers—mostly to the world’s detriment.

Not so long ago, the twin forces of technology and economic liberalisation seemed destined to drive ever greater volumes of capital, goods and people across borders. When the global financial crisis erupted in 2008, that hubris was replaced by fears of a replay of the 1930s. They were not realised, at least in part because the world had learnt from that dreadful decade the lesson that protectionism makes a bad situation worse.

Yet a subtler change took place: unfettered globalisation has been replaced by a more selective brand. As our special report shows, policymakers have become choosier about whom they trade with, how much access they grant foreign investors and banks, and what sort of capital they admit. They have not built impermeable walls, but they are erecting gates.

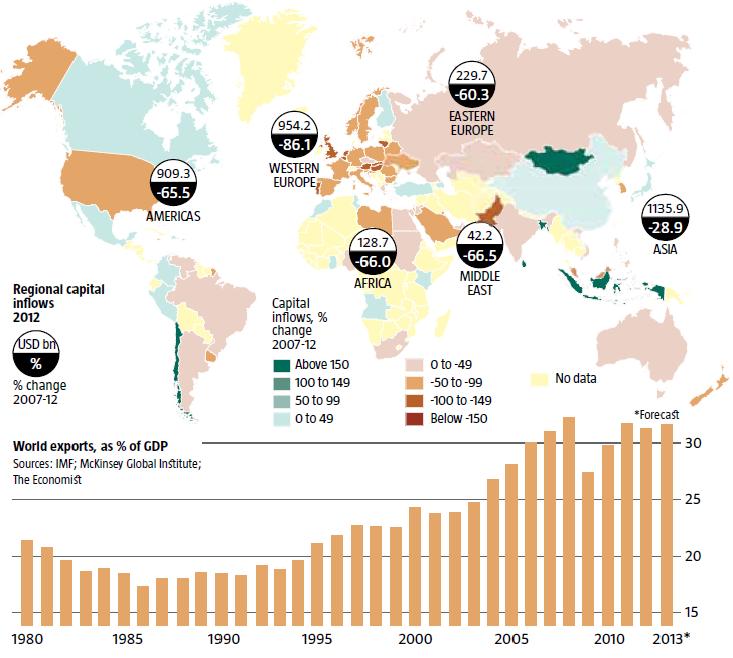

That is most obvious in capital markets. Global capital flows fell from $11 trillion in 2007 to a third of that last year. The decline has happened partly for cyclical reasons, but also because regulators in America and Europe who saw banks’ foreign adventures end in disaster have sought to ring-fence their financial systems. Capital controls have found respectability in the emerging world because they helped insulate countries such as Brazil from destabilising inflows of hot money.

Sparingly used, capital controls can make financial systems less vulnerable to contagion, and crises less damaging. But governments must not forget the benefits of financial openness. Competition from foreign banks forces domestic ones to compete harder. Ring-fencing banks and imposing capital controls protects from contagion, but also traps savings in countries with little use for them.

Trade protectionism cannot claim the justifications that capital controls sometimes can. Fortunately, the World Trade Organisation (WTO), the trade watchdog, prevents most ostentatious protectionism, but governments have developed sneaky methods of avoiding its ire. New impediments—subsidies to domestic firms, for instance, local content requirements, bogus health-and-safety requirements—have gained popularity. According to Global Trade Alert, a monitoring service, at least 400 new protectionist measures have been put in place each year since 2009, and the trend is on the increase.

Big emerging markets like Brazil, Russia, India and China have displayed a more interventionist approach to globalisation that relies on industrial policy and government-directed lending to give domestic sellers a leg-up. Industrial policy enjoys more respectability than tariffs and quotas, but it raises costs for consumers and puts more efficient foreign firms at a disadvantage. The Peterson Institute reckons local-content requirements cost the world $93 billion in lost trade in 2010.

Attempts to restore the momentum of free trade at a global level foundered with the Doha round of trade talks. Instead, governments are trying to do so through regional free-trade agreements. The idea is that smaller trade clubs make it easier to confront politically divisive issues. The Trans-Pacific Partnership (TPP) that America, Japan and ten others hope to conclude this year aims to set rules for intellectual-property protection, investment, state-owned enterprises and services.

Regional free-trade deals are a mixed blessing. Designed well, they can boost liberalisation, both by cutting barriers in new areas and by spurring action in multilateral talks. Done badly, they may divert rather than expand trade. Today’s big deals are probably a net positive, but they may not live up to their promise: in the rush to sign a deal, TPP participants look likely to accept carve-outs for tobacco, sugar, textiles and dairy products, diminishing the final deal.

…but it could be so much better

Gate-building does not cause much outrage. Yet it is worth remembering what opportunities are being lost. In 2013 the value of goods-and-services exports will run to 31.7% of global GDP. Some big economies trade far less: Brazil’s total exports are just 12.5% of GDP. Increasing that ratio would deliver a shot in the arm to productivity. Trade in services is far lower than in goods; and even in goods, embarrassing levels of protectionism survive. America tacks a 127% tariff on to Chinese paper clips; Japan puts a 778% tariff on rice. Protection is worse in the emerging world. Brazil’s tariffs are, on average, four times higher than America’s, China’s three times.

In the past year the cost of impediments to trade has become clearer. Few countries have put up more gates than Russia, India and Brazil; growth in all three has disappointed. The latter two have suffered sharp falls in their currencies. Some countries have counted the cost and are opening up. China’s new leaders are tiptoeing towards looser rules for foreign capital and getting behind a push for a modest global trade deal. Mexico plans to readmit foreign investors to its oil industry in an effort to boost output. Japan hopes that the TPP will shake up its inefficient sectors, complementing fiscal and monetary stimulus.

But the fate of globalisation depends most on America. Over the past 70 years it has used its clout to push the world to open up. Now that clout is threatened by China’s growing influence and America’s domestic divisions. Barack Obama’s decision to skip an Asia-Pacific leaders’ summit in Bali to battle the government shutdown at home was ripe with symbolism: China’s and Russia’s presidents managed to attend. Mr Obama must reassert America’s economic leadership by concluding a TPP, even one with imperfections, and force it through Congress. The moribund world economy needs some of the magic that globalisation can deliver.