Despite the fact that it has been largely forced, and is dilatory and fragmented, the reform of Ukraine’s energy sector has already led to radical changes. The most difficult part is changing the rules of play on the domestic field, ending monopolism, and opening the way to competition among a gradually larger number of companies that are truly independent of each other. After that comes improving the quality of consumer services and preventing, as much as possible, windfall profits among suppliers. Bringing rates to market levels, deregulating them, and reducing dependence on external monopolist suppliers is the only means of providing the conditions for this key component of change that will guarantee the main advantages of reforms for ordinary Ukrainians.

Natural Gas: Enroute to self-sufficiency

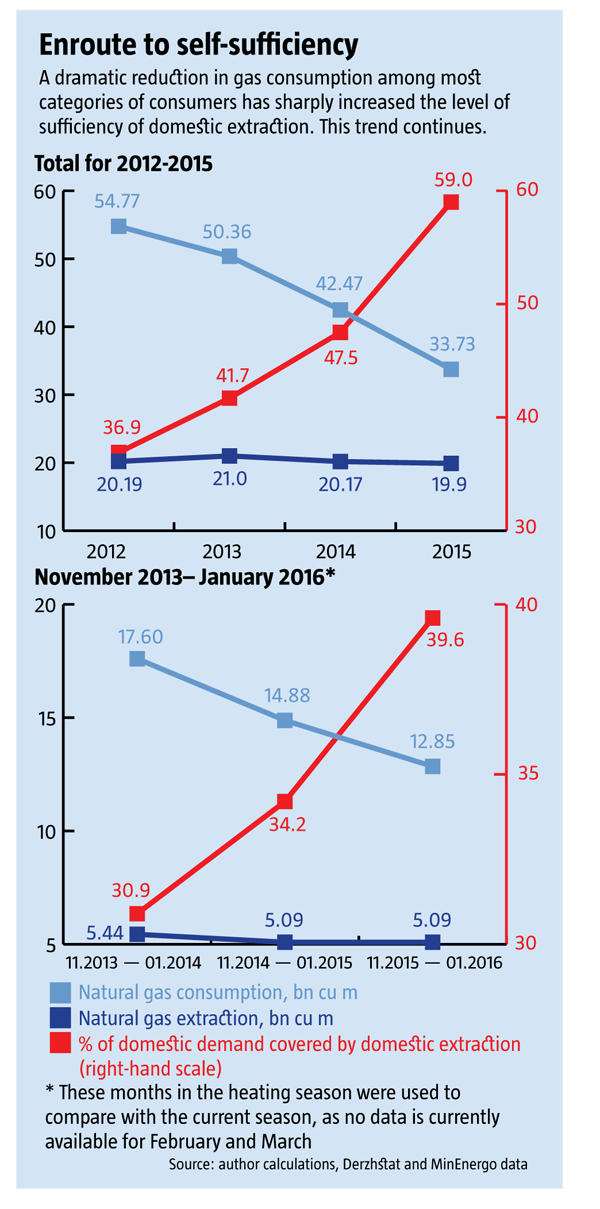

For a long time, improving the country’s energy security was linked to diversifying sources of natural gas imports. However, it turned out that the problem could also be resolved by reducing consumption. In 2015, only 33.7 billion cu m were used, 19.9bn cu m of that domestically extracted, bringing self-sufficiency up to 59%. In fact, it’s actually higher, as considerable amounts of the gas consumed are used to cover the transit of Russian gas to the EU through the Ukrainian gas transport system (GTS), which cannot be rightfully considered “domestic consumption.”

As we can see, 13.8bn cu m of gas were missing to cover domestic demand in 2015, although 16.45bn cu m were imported, “just in case.” Meanwhile, the throughput of the Slovak and Polish pipelines that have been successfully used to buy gas from the EU is over 15bn cu m per year. That is, it’s more than enough to cover current annual demand in Ukraine without buying any directly from Russia.

Last year’s purchases made it possible to establish significant reserves for future use: at the beginning of March, the gas storage system contained more than 10bn cu m, the highest level since 2011, despite the fact that consumption has gone down by one third. If we presume that consumption of gas from March to October 2016 will be somewhat lower than in the same period of 2015, when it was 15.1bn cu m, then projected domestic extraction during these months, 13.5bn cu m, should be suffice for just about all domestic demand. That means that nearly all the volume of gas purchased on the EU market can be used to fill storage tanks. Given the currently low gas prices and the abundance of gas during the warm seasons, Ukraine could be looking at 8-10bn cu m additional reserves over the next 8 months—but only if full capacity is used, and not one quarter, as was the case during the first few days of March, for reasons unknown.

RELATED ARTICLE: British energy expert on the development of Ukraine’s energy system and the Energy Union

This will be enough to meet the next heating season with a surplus no smaller than what Ukraine had at the beginning of this last season. And that means, once again, not having to buy fuel directly from Russia. Even more, there’s every reason to believe that domestic extraction will continue to expand to cover domestic demand.

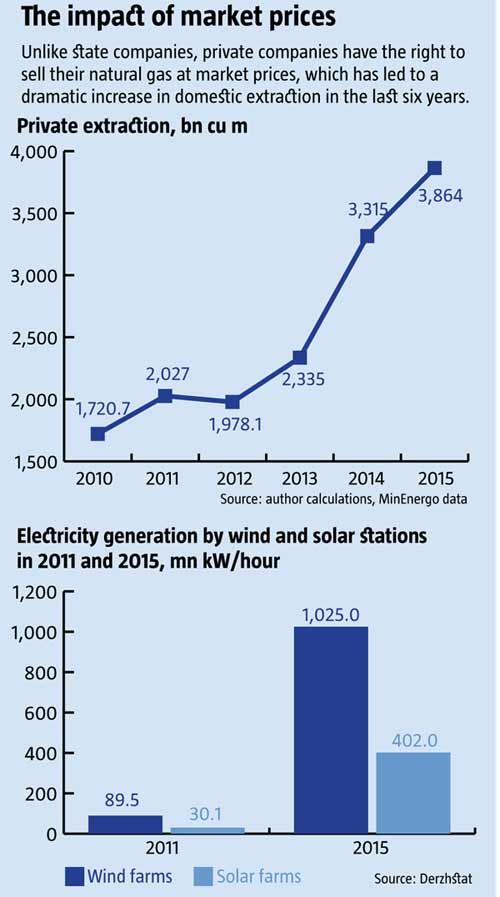

On one hand, this prediction is based on sustained trends to growing extraction by private companies. Their number is rapidly growing on the market and is already high enough to affect the overall balance, even if state companies were to cut output back. In 2015, Naftogaz’s rate of extraction contracted by 823 million cu m, which was faster than extraction by private companies grew—by 563mn cu m. But lately, a breakthrough occurred in the growth of extraction by private companies: In January 2016, they added 69mn cu m, compared to January 2015, while Naftogaz’s extraction declined by only 34mn cu m.

The share of Rinat Akhmetov’s DTEK grew especially sharply, demonstrating that the laws of the oligarchic model of economy are still working. NaftogasVydobuvannia, the natural gas division of DTEK, nearly doubled its output, from 0.75bn cu m in 2014, to 1.3bn cu m in 2015, and has maintained that pace in 2016: in January, output was more than 125.5mn cu m. It looks like DTEK could break through to a 10% share of domestic extraction and 40% of extraction by non-state companies, making it a key player not only on the coal and power markets, but on the gas market as well.

The share of Rinat Akhmetov’s DTEK grew especially sharply, demonstrating that the laws of the oligarchic model of economy are still working. NaftogasVydobuvannia, the natural gas division of DTEK, nearly doubled its output, from 0.75bn cu m in 2014, to 1.3bn cu m in 2015, and has maintained that pace in 2016: in January, output was more than 125.5mn cu m. It looks like DTEK could break through to a 10% share of domestic extraction and 40% of extraction by non-state companies, making it a key player not only on the coal and power markets, but on the gas market as well.

On the other hand, raising gas rates to market levels and improving the subsidy mechanism—at the moment, it simply encourages households to over-consume again—should stimulate an even greater reduction in domestic gas consumption over the next few years. As of March 1, 2016, the price for commercial customers ranges from UAH 7.34 to UAH 8.39 per cu m. In other words, as gas rates are equalized for all categories of consumers, a process that is expected to be completed in 2017, rates for cogeneration companies, currently UAH 3.00/cu m and for residential use, currently UAH 3.60/cu m at a subsidized rate for up to 1,200 cu m/year, have room to grow. The latest stage begins on April 1, according to the Premier, when the subsidized household rate for the first 200 cu m per month could go up from UAH 3.60 to UAH 5.50/cu m, according to NEURC, the National Electricity and Utilities Regulatory Commission.

The rate for cogeneration plants, which were particularly wasteful in their consumption this past winter, forcing residential consumers to effectively heat the out-of-doors because of the unusually high temperatures in centrally heated apartments, is also likely to go up. But here, again, the government will intervene: heating customers have no way to influence the monopolist utility to reduce its consumption of gas. What’s more, cogeneration companies benefit from over-consumption because figures based on ever-more-widespread individual heating meters allows them to issue ever higher bills.

Still, the problem with the cogeneration plants should be resolved positively and a better residential subsidy mechanism should stop wasteful consumption. In a few more years, these two mutually-stimulating trends—domestic extraction increasing by 10-15% to 22-23bn cu m and consumption declining by a similar 10-15% to 28-30bn cu m—, as is projected, could raise Ukraine’s self-sufficiency in natural gas from the current 60-65% to 75-80%. That will reduce the need for imported gas to at most 5-7bn cu m per year, compared to the 35-40bn cu m that Ukraine was buying not that long ago.

So far, this path offers the most realistic and reliable means to shield against the threat that Russia will sharply reduce the volume of gas transiting via Ukraine’s GTS—and possibly eliminate it altogether—by 2020, when the current contract runs out. A steep reduction, not to mention a less likely halt, to the transit of Russian fuel across Ukraine’s territory is likely to complicate purchases from the EU and to make them considerably more expensive. If demand remains at the levels that it is today, this will mean not just substitution, but physical transporting from distant European hubs.

The main threat to Ukraine’s growing self-sufficiency is a potential decline in the price of imported gas to US $150/cu m or less. This would reduce the difference between industrial rates in countries with large domestic extraction capacities, such as Russia and its satellites, and importing countries, which could stimulate Ukraine’s energy-hungry manufacturing to increase output. Still, the general trend in Ukraine’s economy is for the steel, heavy chemicals and machine-building industries to die off as the agro-industrial complex (AIC), labor-intensive industrial production and service industries, including IT, grow, and for the consumption of residential gas to continue to go down. All these trends make it more likely that Ukraine will successfully reorient itself towards self-sufficiency, perhaps not for its entire domestic needs, but for the majority, over the next 4-7 years.

RELATED ARTICLE: What it takes to make changes irreversible in Ukraine

Nevertheless, Ukraine should seriously consider building a terminal capable of handling 2-3bn cu m of natural gas on the Black Sea shore. This would increase the capacity of the domestic economy to withstand external challenges and to take advantage of the opportunities offered by a sharp increase in the liquid gas market expected in the next few years. The shifting geopolitical layout, including the conflict with Russia, Turkey should not be against such an option, while the US, as the most likely alternative supplier, should be interested in supporting such a project.

Power to the power grid

At the same time as Ukraine’s dependence on Russian gas supplies is slowly being overcome, the problem of its dependence on Russia for electricity, both atomic and thermal, is moving to the fore. In 2015, Ukraine imported fuel rods for its nuclear power plants (NPPs) worth US $643.6mn, nearly 95% of those bought from Russia’s nuclear monopoly, Rosatom. Only 5% or US $32.7mn worth was bought from the Swedish subsidiary of the world’s largest atomic energy corporation, Westinghouse.

Energoatom’s dependence on Rosatom has become a key energy security issue for Ukraine. Given a 35-40% dependence on imported gas, of which only 20% comes from Russia, the country is 100% dependent on imports of nuclear fuel, 95% of them from a Russian state-owned monopoly. At the same time, Energoatom’s share of power generation domestically is nearly 50%. The only way out of this situation is to increase the import of NPP fuel rods from western manufacturers to at least 50%, as the current nigh-symbolic 5% is only pretend diversification. That is the first phase. The second is to build a domestic facility in partnership with western manufacturers to produce fuel rods in the medium term.

RELATED ARTICLE: What makes Ukrainians vulnerable to populism

Meanwhile, domestic thermal power plants and co-generation plants (TPPs and TECs) are extremely dependent on supplies of fuel from Russia and ORDiLO, the territories it has occupied in Donetsk and Luhansk Oblasts. According to Derzhstat, Ukraine imported nearly 1.9mn t of heating coal for US $157.5mn, of which 940,000 t came from Russia for US $85.4mn. Yet this is just the tip of the iceberg of how dependent Ukraine’s thermal energy system on risky supplies from outside, because the much larger volumes of coal coming from occupied territories are just as dependent on the goodwill of an enemy as are the volumes coming from Russia.

Moreover, obviously corrupt schemes for buying coal from the terrorists in ORDiLO are being boldly lobbied. Although Ukraine has a genuine shortage of anthracite and the arguments for buying it from Russia and the occupied Donbas appear reasonable, NPP power output is being artificially reduced in favor of the more expensive electricity generated by TPPs. Worse, this trend appears to be growing. For instance, NPPs generated 0.9% or 0.8bn kW•h less electricity in 2015 than they had in 2014 and 3% or 2.6bn kW•h less than in 2011. In January 2016, they were down by 5.2% over January 2015, when domestic TPPs and TECs increased output 9.1%. Total power generated in Ukraine remained more-or-less at January 2015 levels.

Moreover, obviously corrupt schemes for buying coal from the terrorists in ORDiLO are being boldly lobbied. Although Ukraine has a genuine shortage of anthracite and the arguments for buying it from Russia and the occupied Donbas appear reasonable, NPP power output is being artificially reduced in favor of the more expensive electricity generated by TPPs. Worse, this trend appears to be growing. For instance, NPPs generated 0.9% or 0.8bn kW•h less electricity in 2015 than they had in 2014 and 3% or 2.6bn kW•h less than in 2011. In January 2016, they were down by 5.2% over January 2015, when domestic TPPs and TECs increased output 9.1%. Total power generated in Ukraine remained more-or-less at January 2015 levels.

The main argument in favor of buying coal from the occupied territories is the low price of about US $45/t, when South African coal costs $70-75. Still, by buying coal from ORDiLO, Ukraine leaves its power industry vulnerable to blackmail by an enemy and finances a war against itself. Information from the occupied territories suggests that the terrorists keep at least 20-25% of the value of the coal that is shipped to Ukraine through “taxes” on its sale, on the wages paid to the miners, and on the retail sales that the same miners spend their wages.

Meanwhile, Ukraine itself has growing problems selling steam coal. The territory under Ukraine’s control is capable of extracting more than it is currently doing, but there is no market for it. By modernizing at least half of the anthracite power blocks to switch to this type of coal could resolve the problem of selling at least 10mn more tonnes of domestic coal and end the dependence on uncertain supplies from both Russia and occupied Donbas.

Yet this process has been sabotaged for over a year at this point. Even at the still state-owned TsentrEnergo, reconstruction has been started on just two of the 10 power blocks at the Zmiyiv TPP. This will allow for less than one fifth of the consumption of anthracite, which is no longer extracted in Ukraine, to be substituted. Meanwhile, the biggest power company using coal from the occupied territories, DTEK, has no intention of reconstructing anything as it anyway sells huge volumes of power on the domestic market.

Switching thermo-electric power to steam coal would give Ukraine’s critical electricity industry a second chance, open the way to reorient on domestic generation, just like the gas industry, and make balancing the energy market an indispensable instrument. All the other types of power generation may have their various advantages, but none of them are in a position to sharply increase output at peak demand times or to reduce it when there is an oversupply. This problem arises for not just NPPs, but also alternative forms, such as wind power and solar energy.

Alternative energy stations currently generate small amounts of power for the grid, but they are growing rapidly. For instance, power generation from solar energy stations (SESs) grew 13.3 times, even with the loss of the Crimean farms, which had provided more than half of Ukraine’s solar power in 2013. Similarly, wind farms (VESs) generated 11.5 times more power in 2015 than in 2011, although a large chunk of their capacities were also lost in Crimea and Donbas. The spread of “green” rates to family solar and wind farms that sell power to the national grid has provided incentives for people to actively set such alternative energy generation up on their private farmsteads. As a result, the number of registered family generators grew nearly 12 times in 2015 and the power they generate was up 10 times, to 0.41mn kW•h.

One of the drawbacks of solar power is, of course, its unpredictability. For instance, in June and July 2015, when less power is needed because it is summer, they produced 46-50mn kW•h of power a month, whereas in winter, when demand is high, they generate far less—only 10.8mn kWh in January 2016. Wind power is not much more reliable: even during the course of a single season, output fluctuated more than 150%: from 54mn kW•h in July to 88mn kW•h in August. And that does not even take into account fluctuations at different times of the day.

In short, the high cost of power and the fact that it is still impossible to control the volumes generated in response to consumer demand, alternative energy will not be able to replace atomic or thermal energy for the foreseeable future, although it promises to rapidly increase its contribution—so far less than 1%—to Ukraine’s power grid.

Follow us at @OfficeWeek on Twitter and The Ukrainian Week on Facebook