The European gas market and the architecture of its supply routes are undergoing tectonic changes, after which it will never be the same as in previous decades. Therefore, it will be impossible for Ukraine to take the same place and play the role that it did in the previous configuration. Attempts can be made to slow the process down, but it is impossible to stop. In addition, the perennial passivity of Ukraine inexorably leads to it being pushed to the periphery.

The chance to become the centre of the new gas architecture – a diversified hub through which the fuel would be delivered from different sources (not only Russia, but also Azerbaijan, Turkmenistan, Iran, etc.) – has already been snatched away to Turkey. In recent years, Ukraine has even been renouncing this role to Poland, which has built a LNG (liquefied natural gas) terminal on the Baltic coast to accept shipments from Qatar, the United States or any other country and is preparing to build a pipeline from Norway.

Holding on to Ukraine’s status as the main transit country of Russian gas at any price would be both dangerous and naive. Firstly, this could only happen if the Ukrainian GTS is fully transferred under the control of the Russian Federation and consent is given to vassal-like dependence on the latter in the political sphere. Secondly, even under such conditions, Russia would seek to diversify its supply routes to eliminate any risks of dependence on another country, even a loyal one. This is clearly demonstrated by the experience of Belarus, whose transit potential in supplying Russian gas to the EU has been put on the back burner for many years in favor of developing new lines of Nord Stream. Full control of Gazprom over its GTS and a pro-Russian orientation have not helped Minsk.

RELATED ARTICLE: Shadow-boxing: Kramer vs Lutsenko Is Ukraine’s halted cooperation with Mueller investigation linked to the seeking of U.S. missiles?

Against this background, more and more flows of natural gas will bypass Ukraine. Over the last decade, the share of Russian fuel transported to the EU through the Ukrainian gas transmission network has  decreased from 70-80% to 44% in 2017 and in the coming years it is supposed to drop to 10-20% or, at worst, a negligible amount. In the meantime, about 25% of transit now takes place through Belarus and 30% via the active part of Nord Stream. In the fourth quarter of 2017, Ukraine's share of transit dropped all the way to 39% due to an increase in the use of Nord Stream, which reached 100.7% of its nominal capacity.

decreased from 70-80% to 44% in 2017 and in the coming years it is supposed to drop to 10-20% or, at worst, a negligible amount. In the meantime, about 25% of transit now takes place through Belarus and 30% via the active part of Nord Stream. In the fourth quarter of 2017, Ukraine's share of transit dropped all the way to 39% due to an increase in the use of Nord Stream, which reached 100.7% of its nominal capacity.

Gazprom is not only on the home stretch of Nord Stream 2 development, which should double the capacity of the Baltic route, but is also completing the construction of the first line of the Turkish Stream along the bottom of the Black Sea. The latter is capable of putting an end to the transit of Russian gas through Ukraine to not only Turkey, but also at least several neighbouring EU countries that now receive it via Ukraine. In fact, by the third week in April the Pioneering Spirit pipe-laying vessel was only 30km away from the point where the Turkish Stream will come ashore near Kıyıköy. Completion of work on the seabed for the first line, which has a capacity of 15.75 bcm (billion cubic metres), is expected as soon as in early May. Although the further route of the gas pipeline from Turkey to Europe is still uncertain, at the very least Bulgaria and its neighbours in south-eastern Europe will be able to receive Russian fuel through an already existing gas pipeline system. In particular, those that previously supplied fuel to the region and western provinces of Turkey through Ukraine (the Trans-Balkan gas pipeline with a capacity of 12 bcm). For example, in 2017 Bulgaria and Romania alone received 4.5 bcm of transit through Ukraine and Greece another 2.93 bcm. This is almost half the capacity of the first line of the Turkish Stream, although most of the gas from it should go to Turkey.

While Gazprom is diversifying its supply routes to the EU, the EU and its individual member-states are actively working to vary their own sources of fuel. German Chancellor Angela Merkel was right when she recently commented on the Nord Stream 2 issue to say that regardless of how Russian gas is supplied to the EU – along the bottom of the Baltic Sea or through the Ukrainian GTS – this will not in itself increase or decrease dependence on Russian gas.

What Nord Stream 2 could do is undermine European unity and increase Gazprom's capabilities for exerting pressure on individual countries, especially former transit partners. However, a real decrease in dependence on Russian gas does not depend on whether or not it is built, but on whether the supply of fuel from other sources will increase. The EU is working on this. For example, in order to ensure the supply of Caspian gas from Azerbaijan via the Southern Gas Corridor, the German government is preparing to lend EUR 1.2 billion to an Azerbaijani state-owned enterprise through a German bank. Moreover, in October 2017, the European Investment Bank (EIB) also released information that it had allocated US $1.3 billion for the construction of this very route.

Imports of LNG to the EU are also growing – there was an increase of 12% in 2017 and even 16% in its fourth quarter compared to the same periods in 2016. The main suppliers here are Qatar, Nigeria and Algeria, but fuel supplies are also increasing from new sources, such as the United States or Trinidad and Tobago. However, LNG is bought most enthusiastically by Mediterranean countries in the EU, for which pipeline transportation from Russia or Norway is more expensive due to the long distance. In November 2017, the Polish PGNiG announced a 5-year contract with Centrica for the supply of American LNG. At the moment, however, US supplies to the European market are still very low and the Americans prefer other markets due to higher returns there. For example, in 2017 the US exported an equivalent of 17.2 bcm of LNG, of which only 2.2 bcm came to the EU, while almost 60% went to Asia and the remainder to Latin America (26%).

What to do

Ukraine alone is not capable of stopping Russia's bypass routes, and here it really has to rely entirely on the position of the EU and especially the US, for which it is important to stop this project both geopolitically and economically. If active diplomatic opposition does not work and construction of Nord Stream 2 starts after all, sanctions against companies that participate in it will remain one last argument in Washington's arsenal.

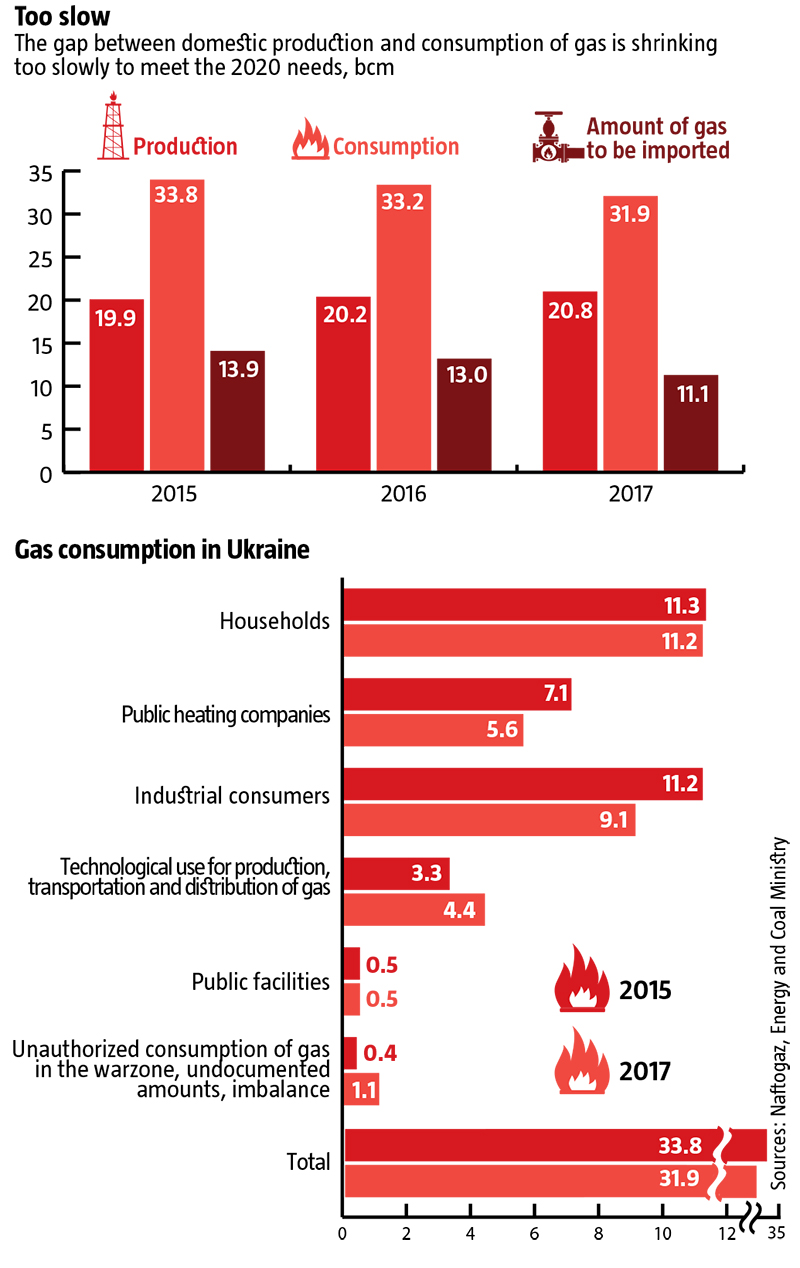

However, Ukraine still holds sufficient tools for internal actions to minimise threats to the country even in the event that Russia's bypass gas pipelines are completed. After all, the loss or a sharp decrease in the transit of Russian gas through the Ukrainian GTS would mainly lead to financial losses. But the inability to satisfy demand for the fuel due to a shortage of domestic gas production, which currently covers one third of consumption and is slowly decreasing, is a challenge to national security.

If the large-scale transit of Russian gas through the Ukrainian gas transmission system comes to an end, purchasing the necessary volumes from EU companies under the virtual reverse flow scheme could become a problem. Transportation from further afield – from routes like TANAP – or purchases from liquefied gas terminals on the Baltic coast of Poland or the Mediterranean in Croatia cannot be considered the best option. Indeed, the cost of such gas in Ukraine would be significantly higher than in other European countries, making a significant proportion of Ukrainian manufacturers uncompetitive.

The best option for Ukraine in these new circumstances is to get rid of the need to import natural gas at all. It seems that this has been declared at the governmental level. However, the problem is that in practice everything is quite different. Measures to save energy and money or increase fuel extraction are still funded residually or blocked by administrative intervention. For example, local authorities sabotage the provision of necessary permits for the increase of domestic gas production by the largest player in the sector, the state-owned company UkrGasVydobuvannya [Ukrainian Gas Extraction].

RELATED ARTICLE: Baby steps to success How Ukraine’s joint ventures with EU countries in the energy sector develop

As a result, after a slight increase in production in 2016-2017, since February 2018 the gas industry has returned to reducing production (1.59 bcm instead of 1.6 bcm in the same month of 2017 and 1.61 bcm in the same month of 2016), which continued in March (1.74 bcm compared to 1.78 bcm in March 2017).

Ukraine’s leadership demonstrates its inability or reluctance to counter the sabotage of plans to increase gas production by local representations of the central government, or equally undermines the activities of individual companies that are associated with political rivals. For example, UkrNafta [Ukrainian Oil] reduced its volume of gas extraction by 17% in 2017 – from 1.3 to 1.1 bcm. The main reason for this was the fact that the State Geology Service blocked the extension of the company's special permits. The volume of gas extraction by private producers in the same year also decreased to 4.1 bcm from 4.2 bcm, although in previous years they had dramatically increased their performance.

Even worse is the situation with decreasing gas consumption. Since 2015, it has remained almost unchanged: according to Naftogaz, the national oil and gas operator, consumption in 2017 fell by only 6% – from 33.8 to 31.9 bcm. This decrease mainly came from the industrial sector, whereas the municipal and household sector has the biggest potential for savings. For example, according to official data, in 2017 households consumed practically the same amount of natural gas (11.3 bcm) as in 2015 (11.2 bcm). This is especially surprising when one looks at regional heating plants reducing consumption by more than 20%, from 7.1 to 5.6 bcm over that period.

Yet again fertile ground has appeared for abusing price differences for certain categories of consumers. While fuel for municipal needs is sold at UAH 6.94 per cu m, the price of gas for commercial customers in May 2018 will amount to UAH 9.14-10.04 per cu m, depending on their volume of consumption and status with debts and prepayments. The loophole whereby fuel can be written off as that used for household consumers at US $100 cheaper per thousand cubic metres creates a breeding ground for corruption and inhibits energy savings. So does the current ill-conceived subsidy system, which provides no adequate incentives for energy conservation or the resources that Ukrainian citizens need to do this, including loans.

The old system of cross subsidization within Naftogaz, which until 2013 provoked wasteful energy consumption, is currently simply implemented through the state budget in a slightly different way. Naftogaz pays tens of billions of hryvnias in taxes and rents from domestically produced gas at prices close to market level and then these funds flow to consumers through the subsidy mechanism of the Ministry of Social Policy.

Over the past few years, a black hole in the market has been growing, made of losses during transportation and distribution, imbalances and so on that are written off, which in the case of Ukraine were already sky high compared to international standards. From 2015 to 2017, 5.5 bcm of gas was written off in this way, compared to 3.7 bcm in 2015. Representatives of international organisations in Ukraine are already taking about this problem without mincing their words. In particular, the managing director of the European Bank for Reconstruction and Development (EBRD) in Eastern Europe and the Caucasus, Francis Malige, frankly stated recently that "A lot of gas still 'goes missing' during distribution. In saying this, I don't mean that it goes missing for everyone. Too much gas is still being stolen during distribution."

Therefore, it is obvious that the plans to reduce consumption and increase production that would give Ukraine a chance of reaching self-sufficiency in the gas sector by the 2020-21 heating season cannot be realised. This, in turn, shows not only the need for decisive steps to intensify the reduction of fuel consumption in the domestic sector and increase of production by private companies, regardless of their ownership. It is also necessary to prepare insurance mechanisms to cover the time lag between the probable suspension of large-scale transit on the Ukrainian GTS – and consequently the virtual reverse flow scheme – and Ukraine's achievement of self-sufficiency in the gas sector by balancing domestic production and consumption at approximately 25 bcm per year.

In this regard, it is already necessary to make a commitment at the state level to fill Ukrainian storage facilities to a maximum level and create a strategic resource while gas is still passing through the Ukrainian GTS in large volumes. After all, if Ukraine could bring reserves in its underground gas storage to 30 bcm before the start of the 2019-20 heating season, a reduction in consumption and increase in production would make it possible to provide the country with the fuel at least until the end of the 2021-22 heating season, or maybe even 2022-23.

This time – almost three years after the probable end of the transportation of large volumes of Russian gas via the Ukrainian GTS in 2019 – should be enough to find an acceptable alternative to imported fuel. Or to balance production and consumption in a way that makes it possible to get through the 2022-23 heating season and all the following with ease.

If it is not possible to fill storage facilities to the brim before the start of the 2019-20 heating season, the country may face serious problems with fuel provision by late 2020. Preparing for them under time pressure will be much more difficult and more expensive, potentially leaving Ukraine vulnerable to blackmail from Russia.

At the moment, Naftogaz is pursuing a diametrically opposed policy aimed at maximising short-term financial gain (less reserves means less funds held up and no procurement means more savings) to the detriment of the country's long-term energy security. At the end of this year's heating season – April 2018 – reserves in the country's UGS facilities were at one of the lowest levels in recent years. Ukrtransgaz, the national gas transmission and storage operator, boasts that "Ukraine started 2018 with its largest underground gas reserves for 5 years – 14.7 bcm. This made it possible to successfully get through the 2017/18 autumn-winter period with its record long-lasting low temperatures in March this year, as well as reduce the need for gas imports from the EU during a period of traditionally high prices at European hubs."

From a solely corporate perspective, this policy from Naftogaz leadership may be correct. Therefore, political decisions and the will of the country's leadership are needed to entrust Naftogaz to act as an agent of the state in guaranteeing long-term energy security and forming the maximum possible strategic reserves of natural gas in UGS. There is still time. Reverse flow capabilities make it possible to accumulate up to 30 bcm of the fuel in Ukrainian storage tanks by November 1, 2019. However, every month of delay in decision-making will increase the cost and make the performance of this task more technically complex.

Translated by Lidia Wolanskyj

Follow us at @OfficeWeek on Twitter and The Ukrainian Week on Facebook