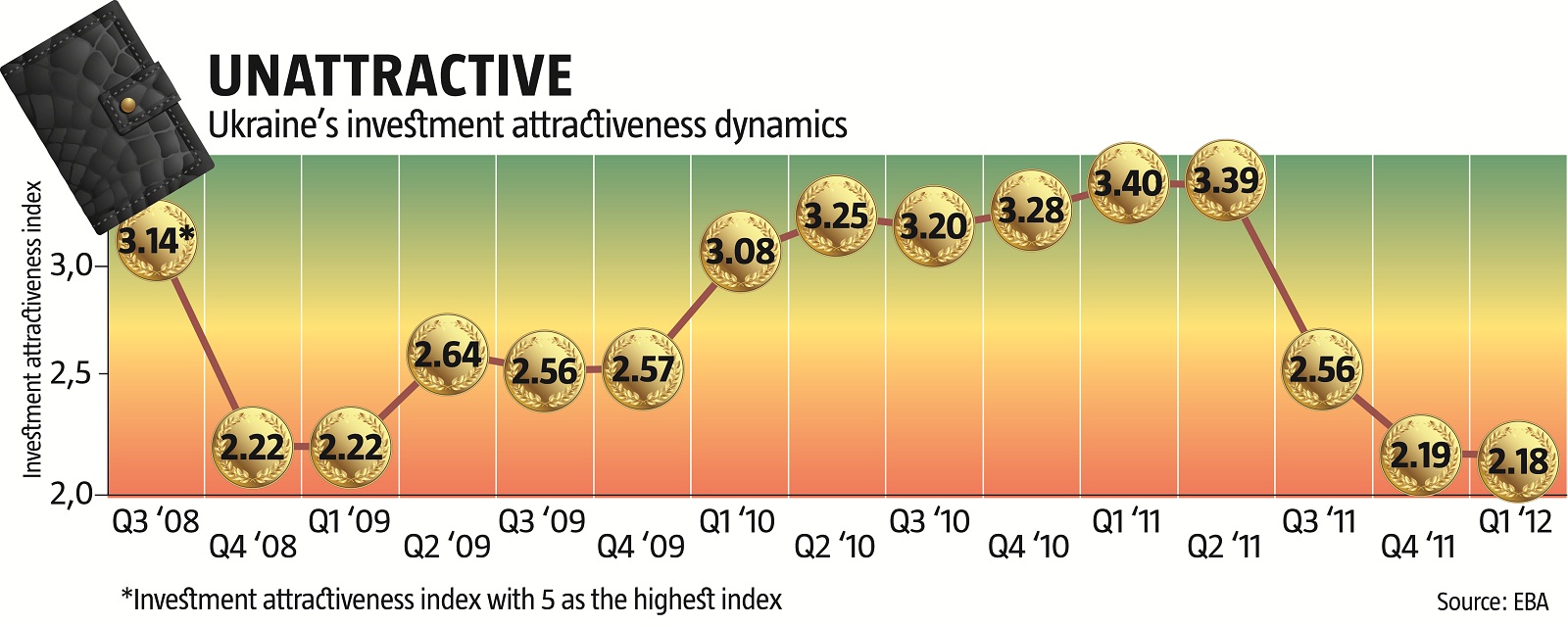

The latest Investment Attractiveness Index, compiled by the European Business Association (EBA) on a quarterly basis since 2008, once again does not look good for Ukraine. In the first quarter of 2012, investors gave the Ukrainian business climate a rating of 2.18 out of 5.

Ever since investors estimated their confidence for the Ukrainian market at 2.19 at the end of 2011, which was the worst grade given since the creation of the survey, there has been no steep improvement or decline in Ukraine’s business attractiveness. What looks troubling, though, is that the index continues to decline, if only slightly.

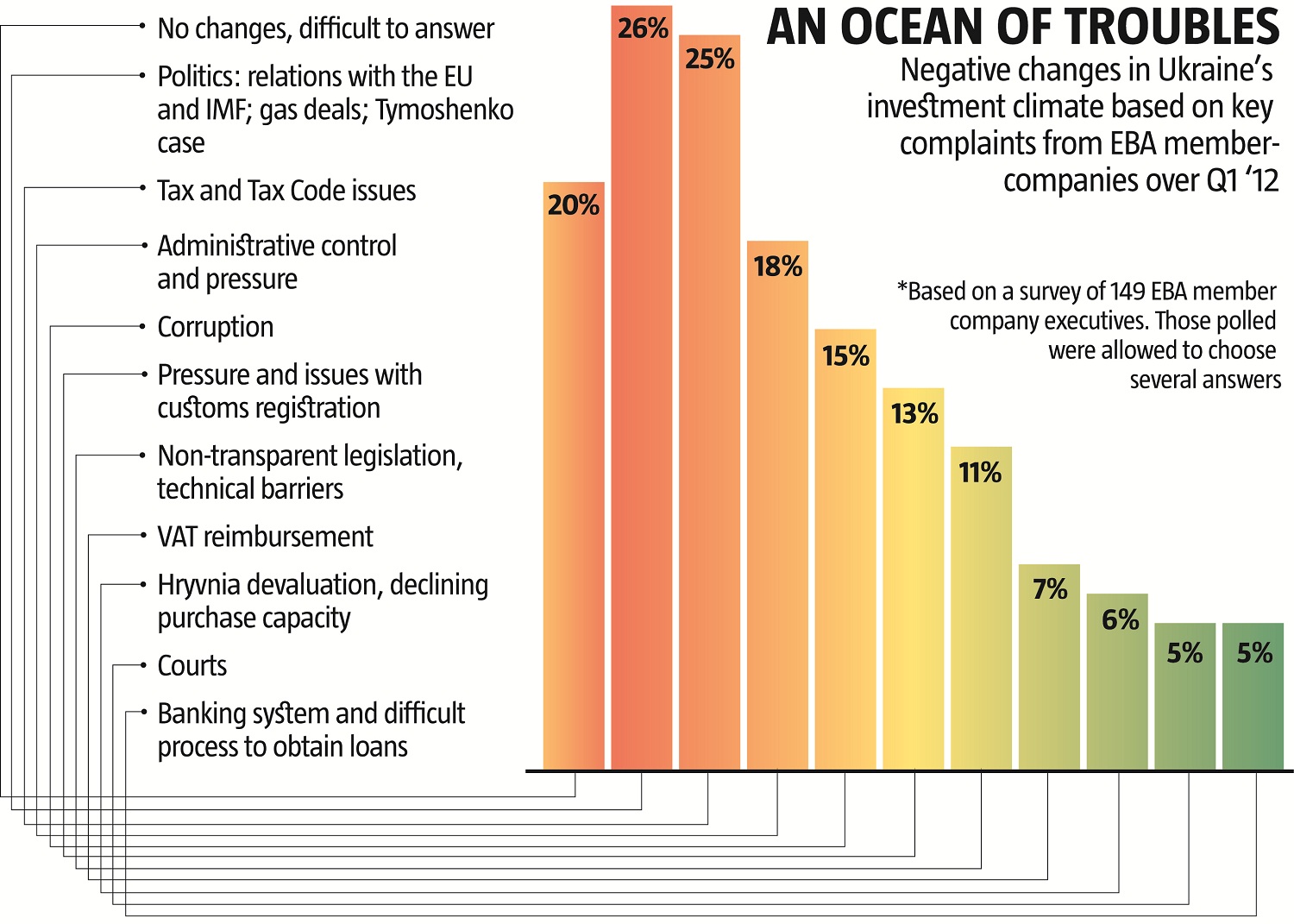

What is spoiling the investment climate? The key factors listed by EBA member-company CEOs include chronic problems on the Ukrainian market, such as an imperfect and non-transparent legal framework, corruption, red tape and excessive government interference in business. In addition, the investor survey shows that with relations between Kyiv and the EU cooling down, Yulia Tymoshenko incarcerated, and an unstable foreign policy, the country’s political situation reinforces investors’ negative attitudes toward Ukraine.

Similar to any chronic disease that requires prolonged comprehensive treatment, each of these problems can be solved through careful reforms and strategic approaches oriented at long-term success rather than a short-term or nominal effect. The business community still has high expectations for the Ukrainian government’s ability to eliminate these problems. Yet, it must first see specific positive steps toward the resolution of key problems in order to believe that the government is serious about improving the investment climate in Ukraine.

Having analyzed numerous complaints from over 900 EBA member companies from all sectors of the economy, we have come up with a slew of common problems that hamper free and productive business operation in Ukraine. Listed below are some possible moves to overcome these barriers.

ACCEPT THE CE MARKING

Ukrainehas not yet accepted the European CE quality marking in legislation. As a result, Ukrainian importers currently face additional burdensome and obsolete procedures to confirm the quality of products and certify goods that have already undergone the necessary testing in the EU. To eliminate this problem and make it easier for importers, the EBA recommends implementing the CE marking for medical products, home appliances and other products through legislation, and making the relevant amendments to Ukraine’s technical procedures.

ADJUST MARKING REQUIREMENTS TO MEET THE RELEVANT EU STANDARDS

The effective rules governing the marking of food and non-food products in Ukraine are rarely harmonized with the relevant EU standards. This makes foreign trade more complicated and affects the moods of investors.

First and foremost, this problem is reflected in the marking of genetically modified organisms. After thorough analysis of the problem, the EBA recommends marking food that actually contains genetically modified organisms (GMOs) rather than the food that does not, as is done currently. This would make the GMO marking procedure in Ukraine fully compliant with EU Directives and practices and cause no excessive obstacles or difficulties for food producers and importers.

REIMBURSE VAT

The problem lies in VAT amounts declared and confirmed for reimbursement by the government, yet never actually reimbursed. The issue of whether the government will meet its VAT reimbursement liabilities is acute at this point and needs to be solved as soon as possible.

What can the government do to fix the VAT reimbursement mechanism and eliminate the debt it has accumulated? We recommend looking at the efficiency of fiscal authorities first and foremost, and focusing their efforts on discovering tax gaps rather than transferring the task to prudent taxpayers or applying the mechanism of writing off VAT amounts applied and confirmed for reimbursement earlier.

FULLY IMPLEMENT THE ELECTRONIC CUSTOMS DECLARATION SYSTEM AND USE UKRAINE’S TRANSIT POTENTIAL EFFECTIVELY

Electronic customs declaration is a modern mechanism that simplifies customs processing and trade if used properly. However, it has not been fully implemented, and can therefore not be used 100% effectively. The transition to electronic document processing for other regulatory authorities that issue customs documents or still use paper customs declarations would substantially simplify foreign trade transactions in Ukraine. As a result, the use of electronic customs declarations failed to simplify foreign trade transactions significantly. For instance, the process does not allow electronic customs declarations to be filed to a bank to make transnational settlements under the relevant currency control.

DEVELOP TRANSIT POTENTIAL

In addition to the limited use of electronic customs declarations, other factors hamper the efficient use of Ukraine’s transit potential. Transit potential includes the effective use of “transit storehouses” where goods for foreign markets are stored and the lack of legislative procedure for such import-export transactions. These problems stem from regulation. Today, banks cannot perform settlements under foreign trade transactions beyond foreign exchange controls based on customs declarations for products placed in a storehouse, even though that is how transit storehouses operate when products are brought into a country, duty and VAT free, for subsequent export to another country. Today, any companies intending to perform this transaction must import the goods, pay all import duties including VAT, then register an export transaction and look forward to VAT reimbursement later.

The EBA has drafted a series of amendments and recommendations for the NBU and State Tax Service regulations to provide for the full-scale operation of re-exports.

ALLOW TAX LOSSES FOR EARLIER PERIODS TO BE CLAIMED

Unfortunately, the new Tax Code does not solve the problem of taxpayers claiming tax losses for earlier periods. The lack of practice and mechanisms to solve this problem results in uncertainty and tension between taxpayers and fiscal authorities.

Having studied the experiences of Russia and EU in this matter, the EBA notes that taxpayers should have a right to claim tax losses for earlier periods in full in their tax statements and any restrictions, if implemented, should be temporary.

REGULATE TRANSFER PRICING

Ukrainehas no regulation framework for transfer pricing. This breaks the rules of fair competition and can unbalance the market. Together with top experts, the EBA has drafted a concept to amend transfer pricing legislation. It provides for the drafting and passing of laws regulating transfer pricing enforcement, documentation, sources of information on prices and so on.

Finding solutions to all of these technical issues is a realistic objective that would not require excessive amounts of time or effort. The EBA will continue to seek solutions to the so-called global problems of the Ukrainian economy. Yet, the current situation makes its own rules, therefore we are focusing on solving simple yet crucial issues for the business sector. From individual elements, we can build the foundation for a transparent, attractive and stable investment field in Ukraine. Success comes in the details.