Self-composed and most of the time independent, Premier Mykola Azarov has recently announced that Ukraine will ask for a new IMF tranche to repay their previous loans. Rumours have surfaced, that Yuriy Kolobov, the newly-appointed Finance Minister, will soon be visiting the USA to negotiate debt restructuring with IMF representatives. Open sources have published unconfirmed information about requests of the Ukrainian government for high-standing US lobbyists to arrange for a bridge to the IMF to get a new tranche without raising gas prices for the public in Ukraine. What is happening here?

In February, Ukraine repaid an astounding USD 575mn to the IMF, both on time and in full. Later, in a video address posted on the central bank’s official website, Olena Shcherbakova, Director of the General Department for Monetary Policy at the NBU, said that the loan “was repaid… with no further complaints from foreign investors, including the IMF”. Surprisingly, this was followed by the above mentioned Premier’s statement – right after Bloomberg analysts estimated that default risks in Ukraine were higher than in any other state other than Greece. Even Argentina has a lower default risk with the price of its five-year credit default swaps 12bp lower than that of Ukraine’s derivatives at 780bp.

HUGE DEBT

2012 will be the year of peak repayments of Ukraine’s accumulated debt. According to the Finance Ministry total government debt, estimated in hryvnia as of December 2012, will hit UAH 415.326bn (USD 51.92bn), or 27.6% of GDP. As much as UAH 95.5bn (USD 11.9bn) will have to be allocated from the state budget. For the most part, the funds will be spent to repay a UAH 16.2bn (USD 2.02bn) debt to Russia’s VTB Bank and UAH 24.8bn (USD 3.1bn) to the IMF, although that is only the tip of the iceberg.

According to the NBU, total short-term foreign debt with a remaining maturity over nine months increased by USD 3.1bn to USD 52.6bn. Exactly this amount of foreign currency may flow out of the country if the debtors demand full repayment of liabilities from the government and Ukrainian residents on 30 September 2012. Even if inter-corporate loans make up the lion’s share of the sum, the rest may turn out to be the equivalent of Ukraine’s foreign-exchange reserves. In previous years, this was hardly a concern as debts were restructured and rolled over worldwide. Yet, only the naïve believe that this process will last forever and the IMF is signaling that it won’t.

The 2012 Budget provides for drawing UAH 38bn (USD 4.75bn) in foreign loans and UAH 61bn (USD 7.6bn) in domestic loans in the current year. According to many polled experts, these numbers signal the government’s optimism rather than realistic expectations. “Ukraine has to repay nearly UAH 13bn (USD 1.6bn) over January-March, while it has borrowed only UAH 5-6bn (USD 0.6-0.7bn) so far,” says Oleksiy Zholud, an analyst at the International Centre for Policy Studies, whose estimates look the most optimistic of all. Mr. Zholud claims that the government is preparing to issue Eurobonds worth USD 1.5bn and it looks like there is sufficient demand for them, yet causes for pessimism are likely to multiply if the plan fails for some reason.

“The Eurozone is in mild recession,” Olli Rehn, European Commissioner for Economic and Financial Affairs, said in an interview for Agence France-Presse. Based on the outcome of 2011, the EU economy has grown 1.5% compared to 1.4% for the Eurozone’s economy. Recession is unfolding not only in Greece, but in Italy, Portugal, Belgium, Netherlands, Czech Republic, Slovenia and so on. As a result, Ukraine will have a hard time finding buyers of its sovereign debt, especially if its relations with the IMF take a turn for the worse. The government realizes this, thus it is looking for cash on the domestic market. In January-March, the Ministry of Finance issued bonds worth UAH 2.5bn (USD 0.3bn) but that is clearly not enough to make ends meet. The government has even begun preparation for the issuance of foreign currency bonds for the public, but will they attract many buyers? The question looks rhetoric unless these papers are backed by real assets, such as land, for instance.

Oleksandr Okhrymenko, President of the Ukrainian Analytical Centre, remains calm even though he is keeping track of developments: “Despite using its gold and foreign exchange reserves (they shrank by USD 315mn in February –ed.), Ukraine repaid the first tranche of the IMF loan without particular difficulties. It might be harder for Ukraine to meet its liabilities to VTB this year, but the parties are likely to come up with a compromise solution.” New loans taken in 2012 will be used to repay the old ones anyway. The question is how the new loans will be repaid?

THE SHAKY BALANCE

“Ukraine started 2012 with the balance of payments deficit higher than in the crisis years of 2009 and 2010,” Oleksandr Okhrymenko comments. “We used to enter January with a surplus, while this January began with a deficit worth nearly USD 890mn.” According to Mykola Ivchenko, an analyst at the FOREX CLUB group, mid- and long-term debts of the private sector were transferred into short-term indebtedness which is an alarming symptom that most likely reflects global crisis escalation. FDI inflow has shrunk 52.7% year on year. Assumingly, this was due to the many holidays in January. Meanwhile, the outflow of foreign currency reported as trading capital was an astounding USD 2.135bn compared to USD 79mn in December 2011. This essentially undermined the financial transactions account (repayment of trade credits by importers serves as an explanation for the process).

The real economy is declining and the NBU has reported that the domestic economy is operating under low foreign demand. As a result, steel works featured negative output dynamics at -1.4% year on year in November 2011, followed by -4.7% in December 2011 and -1.6% in January 2012. According to official explanations, the drop of output is explained by a high base of comparison in the years 2011 and 2010. According to the NBU’s analytical reports, the output of food companies shrank by 1.9% in January 2012 compared to January 2011, while the textile industry faced a 12.1% decline and the transport sector shrank by 1%. Apparently, factors that caused these trends include the recent “reforms.” The decline in the overall transport system performance, for instance, is interpreted as a result of the 2% cut of railway transportation, while bad weather, meaning cold temperatures, reportedly disrupted the supply of raw materials, such as iron ore, coal, coke and scrap to steelworks. Nobody can be sure that processes in Ukraine do not follow the 2008-2009 scenario should the global crisis unfold, since the structure of Ukraine’s critically export-dependent domestic economy has hardly changed. The only difference now is the bigger share of the agricultural complex in the country’s GDP, yet potential “bad weather” makes it impossible to guess the harvest this year. On the whole, the government has already cut the projected DGP growth from 5% to 3%, while the EBRD gives the same figure as 2.5%.

IMF: PLAYING THE BAD COP

“The NBU offset the negative balance of payments in January by selling US dollars worth UAH 904.4mn,” Mykola Ivchenko says. Yet, it cannot support the hryvnia rate by doing so for a long time. Notably, the regulator did not make any significant interventions to level out currency fluctuations over February. “This signals a good balance of demand and supply on the currency market,” Oleksandr Dubokhvist, Director of the NBU Department for Currency Reserve Management and Open Market Transactions, claims. According to Mr. Ivchenko, the newly introduced requirement for individuals to provide their passports for currency exchange transactions in Ukraine has had a certain impact as the demand for freely convertible currencies has dropped nearly 25% in monthly terms. Still, this is not a solution to all current problems.

The sought-after tranche from the IMF is only a tactical move, but even it brings forth challenges. Through intermediaries or directly through its management, the IMF is hinting more and more often at the possible termination of cooperation with Ukraine unless it makes concessions necessary to get another financial injection. These include a 30% rise in gas prices for the public with a further escalation to its prime cost and a 58% increase for co-generation plants with the ultimate consumer paying the whole price. Otherwise, NAK (Naftogaz Ukrayiny) will run into some serious trouble, IMF analysts claim. To minimize financial risks, the IMF insists on hryvnia devaluation even though the NBU has been supporting its relatively sustainable rate over the past few years. Unless Ukraine complies with these demands it will face the need to service and repay earlier loans. Notably, tenser relations with the IMF can affect the government less than other borrowers, whose creditors view the IMF’s decision as an indicator, even though the government’s share in total foreign debt keeps growing.

“Sadly, the IMF is right,”Oleksandr Okhrymenko comments. “A sustainable hryvnia rate turns out too pricey for Ukraine’s economy as the ruble and euro have devaluated. This weakens Ukrainian exports… The only sensible thing to do is to revive the currency corridor to allow for controlling changes in the dollar rate.” The drawback of this approach is that many in Ukraine view the hryvnia rate as virtually the only sign of stability. Therefore, any fluctuations will immediately fuel inflation expectations.

“A slight hryvnia devaluation to UAH/USD 8.15-8.21 could actually help exporters,” Mykola Ivchenko claims. “Ukraine’s balance of payments is again expected to end up being negative in 2012. Economic conditions of its partner states have deteriorated against the backdrop of the euro zone’s debt crisis and the growth slowdown in China… The grain harvest can also end up being poorer than expected in Ukraine, which will not improve its balance of trade. Meanwhile, Euro 2012 facilitates imports to Ukraine and not only opens new opportunities for the nation.”

Will the government comply with the IMF’s demands to raise price of gas? On the one hand, the situation where gas is cheaper for retail consumers than wholesale buyers in Ukraine seems strange and price leveling would definitely improve Naftogaz’s financial standing. On the other hand, the gas price for the public, similarly to hryvnia rate, is a cornerstone for the government in view of the upcoming election and raising it through higher utility bills, among other things, would be a very bald move by a government whose popularity is plummeting. Yet, Ukraine’s only potential creditors, other than IMF, are Russia and China. Given the recent statements by Kostiantyn Hryshchenko, the Minister of Foreign Affairs, China is currently the big hope of the Ukrainian government: “China is a global power. It has every chance to be a calm and unobtrusive power in the European political arena which is particularly appealing to us.” Similar to the IMF, Russia is also likely to demand the increase of gas prices in Ukraine as a prerequisite for granting Ukraine a loan or other concessions in terms of the economy, culture or education. Economically, Russia is currently in no position for a splurge, but its geopolitical interests remain unchanged. China’s interests are nothing new: lately, China has been buying up government liabilities as part of its strategy of tough protectionism on foreign markets. As it tries to maneuver out of these recommendations, Ukraine might only have its own forces to count on, which it should evaluate realistically.

Many experts see the Euro 2012 as a stabilizing economic factor for Ukraine, as neither exporters nor importers are looking forward to any kind of a decline. Also, the championship can give the government at least some time for real, rather than declarative reforms, including moves to replace imports and shape the domestic market. If it wastes this opportunity, surviving the crisis escalation will be a quite a challenge for the Ukrainian economy. It has to be true that after it a real default looms.

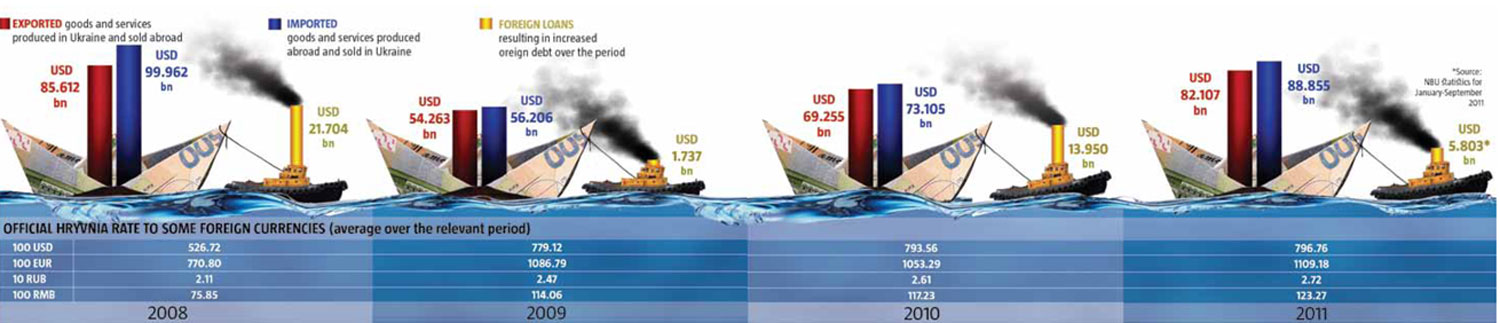

According to the latest statistics, Ukraine exported goods and services worth USD 82.1bn, while importing USD 88.85bn worth of goods and services in 2011. In a number of articles, The Ukrainian Week has pointed out that excessive dependence of Ukraine’s economy on heavy industry ill-fitted the steep decline on foreign markets. At the same time, import is a component of the negative trade balance and problems derived from it, including currency outflow, shrinking output and employment. In upcoming issues, The Ukrainian Week will reveal countries where importers and Ukrainian consumers create jobs and how much this costs Ukrainian economy.

COMMENTS

Will Ukraine plunge into default in 2012?

Serhiy Teriokhin, ex-Minister of Economy

Ukraineis in a pre-default state. The government has to spend almost 1/3 of all budget revenues to repay loans this year. Ukraine is following the Greek way whose government kept taking loans and increasing social spending. With time, it needed more and more money and we all now see the end of all this. The Greek government reported good statistics, yet we are witnessing what is happening now. I realize that there is a parliamentary election soon, and still I’m surprised by the government’s intention to raise social benefits.

Oleksandr Paskhaver, President of the Center for Economic Development

Why don’t we think of possible defaults in Italy, the USA or Russia, for instance? Indeed, the price of Ukraine’s credit-default swaps has grown recently and now only Greek CDSs cost more. But Ukraine is a developing market; therefore it’s always had higher risks. In 2008, the cost of risk insurance for Ukraine was four to five times higher yet no default occurred.