2012 was marked by a liquidity crisis, the maximum squeezing of business for financing pre-election improvements, a worsening of the balance of payments and the hopeless battle of the National Bank of Ukraine against the rising cost of the US dollar. All of this was supplemented with an ever-greater swell of rumours about the Family’s voluntary-coercive acquisition of attractive assets.

As a result – by the end of the year, investors were finally disenchanted with prospects, and most important of all, with the expediency of conducting business in Ukraine. At the same time, the increase in minimum salaries and pensions prior to the election was offset by the problem of their actual payment after election day, which made it impossible to continue covering up the extreme budget crisis, that the Azarov government has led Ukraine into in the last two and a half years.

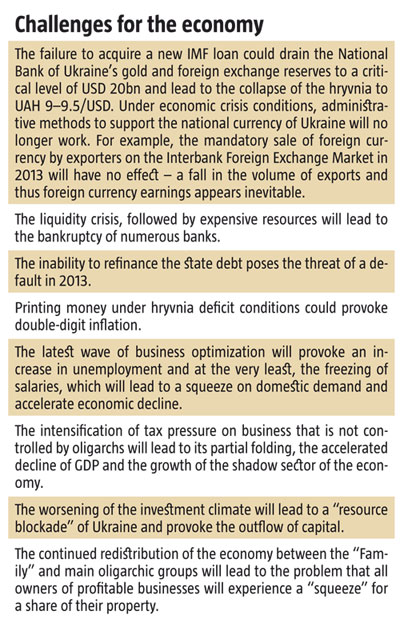

However, taking recent trends into account and the confidence of the ruling regime that it has been on the right course in the last three years, it can be expected that 2013 will be even worse for the economy than 2012 was. The decline of the economies of EU member-states added to the “results” of the Ukrainian government’s activities, as did the obscure prospects for the growth of the world’s heavyweights – the USA and China. Under such conditions, Ukraine has yet to experience a systemic collapse of the hryvnia, manufacturing, etc, which it has been possible to avoid so far with the simultaneous accumulation of disproportion in just about every branch of the economy. Nevertheless, the resources for holding back crisis trends using administrative methods have practically run out.

GDP DECLINE

The gross domestic product (GDP) growth rate, which fell to almost zero in 2012, is very likely to be negative in 2013. There is a high risk of a decrease in the nominal volume of the export of Ukrainian goods, particularly if the world economic situation as pertains export commodities continues to worsen. Eurozone problems will not be eliminated: even the optimistic forecast of the IMF anticipates its economic growth at a level of only 0.2%.

The Russian economy is also slowing down. Its GDP growth rate decreased to 2.9% in the third quarter from the customary 4–5%, while industrial growth (which covers a significant share of domestic export) fell to 1.9% in November, compared to the same month in 2011. The significantly worse 2012 harvest will be reflected in negative macro indices, at least in the first half of 2013 (the export of wheat was de facto suspended in December) – the export of grain substantially improved Ukraine’s trade balance in recent times.

The problem with sales on external markets will supplement the constriction of domestic demand. It’s clear from the 2013 budget that the period of forced increases in nominal salaries and pensions prior to the election has ended.

In 2013, their size remains the same for almost the entire year (until 1 December), thus, under conditions of expected increased inflation, for most of the year, salaries will essentially only decrease. Under conditions of the inevitable optimization of business, which has already begun, the dismissal of a significant number of workers can be expected. All of this will lead to a reduction in the expenses of Ukrainians and subsequently, the decline will not only intensify in branches of industry working for the domestic market, but will also extend to retail trade and the service industry – the last redoubts of economic growth in 2012. Moreover, the greatest decline will be suffered by small and medium-sized business.

Even if a good harvest is gathered and the economic situation improves on external markets in the second half of 2013, this could prove inadequate for the Ukrainian economy to reach at least zero growth by the end of the year. And the methods used by the Azarov/Arbuzov government are not advisable.

BUDGET TROUBLES

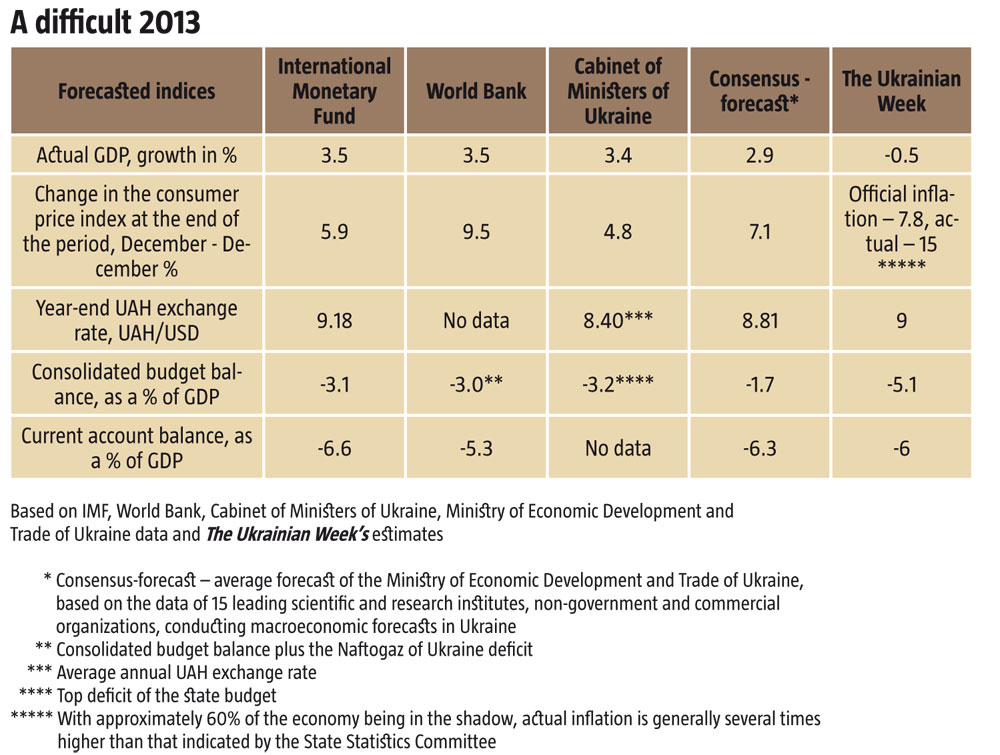

Clearly, budget revenues for 2013 will not be attained. The government’s forecast for nominal GDP in the amount of UAH 1,576bn seems phantasmagorical, but it is the basis for income to the consolidated budget. Statistics show that the 2012 GDP at current prices will probably not reach a level of UAH 1,420bn. Thus, without realistic growth, there can only be a 12% increase of its nominal value in 2013 with a double-digit inflation, which is unrealistic under a stagnant economy.

It’s true that the government has decreased planned revenues to the consolidated budget by UAH 10bn compared to 2012. However, this will not protect the Cabinet of Ministers of Ukraine from the emergence of cash gaps. They will emerge, even in spite of the advance tax payments made by business, and tax rebate indebtedness, which has begun to increase again and even more so in view of these factors. In the worst case scenario, the actual deficit could be twice the size of that planned, although it will accumulate more smoothly than at year-end 2012.

The national debt will also put pressure on the budget. In 2013, Ukraine has to repay USD 9bn in foreign loans and UAH 45bn in domestic loans. Even with renewed cooperation with the IMF, refinancing such amounts as well as financing the planned deficit amount of UAH 50bn will be somewhat difficult. It’s likely that due to the lowering of international ratings, the treatment of the government and private foreign investors, which absorbed almost USD 5bn of government Eurobonds in the last six months of 2012, will worsen. So if the IMF fails to provide funds, the government has no option, other than to print money and/or delay social payments. High inflation, a sharp devaluation of the hryvnia, a fall in the income of the population and the prospects of a technical default towards end of the year is inevitable under such a scenario.

THE SPECTRE OF STAGFLATION

Consumer prices for 2012 have not changed. In 2013, quite a few factors will contribute towards increased inflation. First of all, the expected devaluation “will cause the indexation” of prices on import goods. However, since they only constitute 20% of the consumer basket, even a 20-30% fall in the hryvnia exchange rate will lead to a mere 5% increase in overall price levels. Secondly, it’s very likely that the cost of Iitems with the administrative pricing will increase, particularly in the context of renewed negotiations with the IMF. Thirdly, if the government does not restrict the export of grain, then because of the relatively poor 2012 harvest, a deficit could be seen, as well as a price increase on several food product markets. These factors will go against the flow, which will be determined by a fall in the income of Ukrainians and domestic demand. Therefore the overall level of consumer inflation will not be high. It could be less than the 7.4% check by the IMF, and could possibly not even reach the 4.8% that the government set in the budget. At the same time, the stimulation of the economy through the budget, the financial system or foreign investments, could change the general trend and accelerate the inflation rate, but these resources are currently limited.

It is worth noting that according to a different logic, prices are currently being formed on such markets as real estate, automobile, etc. Efforts to reshape the latter increases risks for dealers. The noticeable narrowing of the market forces them to include ever-increasing expenses into the price. These two factors could lead to more expensive cars, even in spite of the overall decline in the population’s purchasing power. However, the price of real estate and the number of actual agreements will probably decrease. A decline in business activity has already resulted in the business segment stepping up its competition to gain clients, and in time, this trend could also extend to economy class residential real estate.

EXPENSIVE LACK OF FUNDS

Throughout 2012, the cost of loans and deposits was unusually high – the consequence of a permanent liquidity crisis in the banking sphere. Although interest rates were reduced somewhat in December, the systemic reasons for fixing this trend are not apparent yet. Ukrainians could start withdrawing their deposits because of decreased incomes and the exacerbation of devaluation expectations, after the effect of the threat of the introduction of a tax on the sale of currency is exhausted. Moreover, those, who out of panic exchanged a significant part of their hard currency savings, could create an effect of deferred demand, should the threat of devaluation come to pass. Enterprises will withdraw funds from banks because of unprofitable activities and the ever-growing appetites of the tax authorities. On the other hand, foreigners will avoid investing money into an economically unstable Ukraine. So financial institutions will be forced to continue their battle for financial resources, and this will maintain interest rates at a high level for a certain period. Not even a new IMF loan will improve the situation, because in all likelihood, it will only refinance the loans that Ukraine will have to repay in 2013 (about USD 6.25bn).

If cooperation with the IMF is not renewed, then the payment of foreign obligations could bring the monetary mass down to critical levels. Should this happen, there will be record-breaking interest rates, banks could go bankrupt, at which there can be no question of the nationalization of troubled financial institutions, because the government simply does not have the money to bail them out. Deposit and loan rates will probably remain at a high level until the devaluation of the hryvnia, which is inevitable.

DEPLETING RESOURCES

The hryvnia exchange rate was pretty stable throughout 2012, although the disproportion in the balance of payments increased. It is very likely that 2013 will be the year of the devaluation of the hryvnia. The trade deficit will probably stop increasing, but the decreased income of the population will decrease the consumption of imported goods. However, private foreign capital will give such a Ukraine in a wide berth. This trend took root in previous years, and is more detrimental than the current account deficit to the balance of payments. This picture is supplemented with the government’s repayment of the USD 9bn foreign debt, which is planned for 2013. There are two possible scenarios for the further development of events. One: the government comes to a new loan agreement with the IMF. After this, to eliminate disbalance, it conducts a smooth, controlled 20-30% devaluation, which could well be one of the IMF’s conditions. Two: the depletion of gold and foreign exchange reserves at a rate of USD 1–2bn per month and an uncontrolled devaluation of the hryvnia, possibly closer to the second half of the year. In any case, the government does not have foreign currency. Without IMF assistance, at present, it is only possible to acquire foreign currency from Russia, but the cost of this money is well-known. Whether devaluation will then be halted at a controlled and stimulating UAH 9.5–10.50 /USD, or reach a chaotic and ruinous rate of UAH 12 /USD and more, is an open question.